What Is an Annuity? A Comprehensive Guide to Retirement Annuity Investments

Annuities turn your savings into steady retirement income. In Hong Kong, options include public annuities and QDAP, with the latter offering up to HKD 60,000 annual tax deduction. This guide explores their features, benefits, and risks.

TL;DR: An annuity is an insurance product that converts savings into regular income, often used in retirement planning. In Hong Kong, the two main types are the government-backed Hong Kong Annuity Plan and privately issued Qualified Deferred Annuity Policies (QDAP), with the latter offering up to HKD 60,000 in annual tax deductions. Before purchasing, it’s important to assess your financial needs, risk tolerance, and long-term planning objectives.

For many Hong Kong residents, the idea of “a steady monthly income after retirement” is a cherished goal. With an aging population, the average life expectancy for men is 82.5 years and for women 87.9 years (Department of Health data), making it likely that retirees will need to fund over twenty years of living expenses. As a financial tool that transforms capital into stable, periodic income, annuities have attracted increasing interest among local investors in recent years. This article provides an in-depth exploration of annuities—covering definitions, types, benefits, potential risks, and guidance on how to incorporate annuities into a holistic retirement plan.

What is an Annuity? Core Concepts Explained

An annuity is a long-term insurance product. After the policyholder pays premiums to the insurer, the company pays out a fixed annuity income at set intervals starting from an agreed date. Simply put, an annuity converts a lump sum of money into an ongoing cash flow, relieving retirees of the worry their savings might run out.

Annuities differ from general savings or investment products in that their primary function is to provide “income assurance” instead of capital appreciation. Policyholders give up short-term liquidity in exchange for a dependable long-term income source. This makes annuities particularly suitable for retirees seeking protection against longevity risk (the risk of their funds not lasting throughout retirement).

How Do Annuities Work?

At their most basic: the policyholder pays their premium either in a lump sum or by installments. The insurance company starts paying out annuity income monthly or annually from the specified start date, and continues until the end of the policy term or the policyholder's death. The payout period can be for a fixed term (such as 10 or 20 years) or for life.

Main Types of Annuities

Understanding the different types of annuities is the first step to making an informed choice. Annuity products in Hong Kong are generally categorized along the following three dimensions.

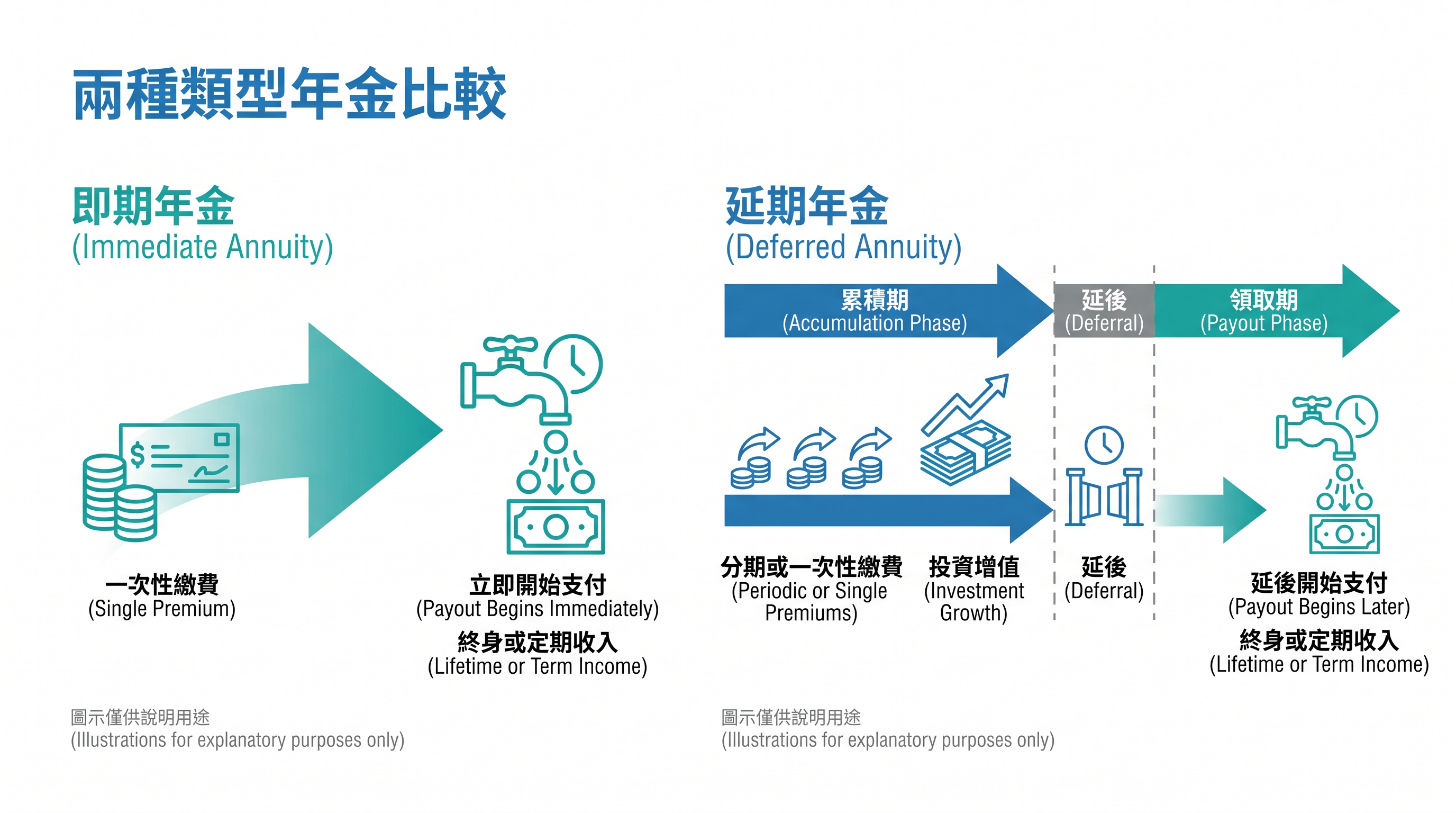

Immediate Annuity vs. Deferred Annuity

Immediate Annuity: After a one-time premium payment, policyholders can usually begin drawing annuity income as soon as the following month. This suits retirees with some savings who need immediate cash flow. The publicly run Hong Kong Annuity Plan (often called the government annuity) is an immediate annuity.

Deferred Annuity: Features an accumulation period in which policyholders can pay premiums in installments or all at once. The capital earns returns during this period, and payouts start from a specified age (usually 50 or above). These products are more suitable for those still in the workforce, looking to plan ahead for retirement. Qualified Deferred Annuity Policies (QDAP) fall into this category.

Life Annuity vs. Fixed-term Annuity

Life Annuity: Pays out as long as the policyholder lives, effectively hedging longevity risk. However, if the policyholder passes away early, the total payouts received may be less than the premiums paid.

Fixed-term Annuity: Has a set payout term, such as 10, 15, or 20 years. The monthly payments are typically higher than for life annuities with the same premium, but the payments stop once the term ends. Note: These may not fully cover the expense needs of exceptionally long lifespans.

Guaranteed Annuity vs. Participating Annuity

Guaranteed Annuity: Income is fixed and guaranteed, unaffected by the insurer's performance or market conditions, making it more suitable for those with a low risk appetite.

Participating Annuity: In addition to guaranteed payouts, these offer potential dividends based on the insurer’s investment returns, providing an opportunity for higher returns. However, the non-guaranteed portion is uncertain.

A Closer Look at the Hong Kong Annuity Plan (Government Annuity)

The Hong Kong Annuity Plan (HKMC Annuity Plan) is insured by HKMC Annuity Limited, fully owned by the Exchange Fund. With government backing, this public product’s primary aim is to provide seniors with reliable, lifetime income.

Eligibility and Premiums

-

Eligibility: Hong Kong permanent residents aged 60 and above

-

Minimum Premium: HKD 50,000 per policy

-

Maximum Premium: Capped at HKD 5,000,000 per applicant

-

Payment Method: Lump sum

According to HKMC Annuity Limited’s official data, with a HKD 1,000,000 premium, a 60-year-old male would receive about HKD 5,100 monthly (approximately a 6.1% payout rate), while a 60-year-old female would receive about HKD 4,700 monthly (around 5.6%). The lower rate for females reflects their longer life expectancy.

Key Features of the Government Annuity

The government annuity includes a premium refund guarantee: if the policyholder dies within the guaranteed term, the beneficiary will receive the remaining annuity payments or a lump sum, ensuring that premiums already paid aren’t forfeited. In addition, policyholders may apply to withdraw the remaining value of paid premiums for medical or dental expenses as needed, with a one-time withdrawal limit of HKD 1,000,000 per person.

Important Note: The Hong Kong Annuity Plan is an immediate annuity and does not qualify for tax deduction under QDAP rules. If you require tax benefits, consider QDAP products separately.

Qualified Deferred Annuity Policies (QDAP) and Tax Benefits

Qualified Deferred Annuity Policies (QDAP) are tax-incentivized products launched by the Hong Kong government to encourage long-term retirement savings.

QDAP Basic Requirements

Per Insurance Authority regulations, QDAPs must meet the following criteria:

-

Minimum Total Premium: HKD 180,000

-

Minimum Contribution Period: 5 years

-

Earliest Annuity Start Age: 50 years old

-

Minimum Annuity Payout Period: 10 years

Tax Deduction Benefits

A major appeal of QDAP is its tax deduction. Each taxpayer can claim up to HKD 60,000 annually for QDAP premiums. At the highest tax rate of 17%, this can save up to HKD 10,200 in tax each year.

Tip: Married couples can each purchase a QDAP, for a combined tax deduction of up to HKD 120,000 per year, with even greater tax savings potential. For further details, consult a licensed tax adviser.

QDAP Returns

Different QDAP products feature differing return structures, typically comprising a guaranteed portion and a non-guaranteed bonus portion. Be sure to review internal rate of return (IRR) disclosures in product information, and note that the non-guaranteed portion depends on the insurer's investment performance and should not be viewed as a fixed return.

Comparison: Government Annuity vs. Private QDAP

| Hong Kong Annuity Plan (Government Annuity) | Qualified Deferred Annuity Policy (QDAP) | |

|---|---|---|

| Type | Immediate life annuity | Deferred annuity |

| Application Age | 60 or above | Usually 18 or above |

| Payout Start Age | Immediately after purchase | Earliest at age 50 |

| Tax Deduction | Not applicable | Up to HKD 60,000 per year |

| Underwriting Institution | Government-backed | Private insurer |

| Return Stability | Fully guaranteed | Partially guaranteed with dividends |

| Death Benefit | Refund of unused premium | Depends on policy terms |

Pros and Cons of Annuities

Main Benefits of Annuities

Mitigate Longevity Risk: Annuities (especially life annuities) ensure policyholders will always receive income as long as they live, minimizing the risk of outliving their savings.

Stable Cash Flow: Regular annuity payouts help retirees manage daily spending with discipline, avoiding financial strain from large lump-sum outlays.

Tax Planning: QDAP premiums are eligible for tax deduction, so you can save on taxes while building retirement funds.

Exemption from Welfare Asset Test: Under current rules, paid premiums and guaranteed cash values in annuity plans are not counted toward the asset limit for Elderly Living Allowance, helping eligible seniors continue to receive about HKD 4,000 per month in subsidies.

Points to Note Before Buying Annuities

Inflation Risk: Annuity payouts are typically fixed, so their purchasing power may erode over time due to inflation. According to the Census and Statistics Department, Hong Kong’s average inflation rate from 2014-2024 was about 2%, which is significant in the long run.

Lower Liquidity: Annuities are long-term commitments; early surrender typically involves a penalty or discounted payout, so you may not be able to recover all your premiums.

Limited Death Benefit: Some annuity products provide death benefits much lower than the premiums paid if the policyholder dies early, making them unsuitable for wealth transfer purposes.

Not a One-Stop Retirement Tool: Annuities are aimed at risk management rather than wealth accumulation, so their internal rate of return is usually lower than higher-growth options like stocks or balanced funds. Consider combining annuities with MPF, stocks, bonds, or other investment products to create a diversified retirement portfolio.

Who Are Annuities Best For?

Annuities are not suitable for everyone, but are particularly relevant for:

Nearing or Recent Retirees: Those approaching retirement, with some savings who want to convert part of their funds into a fixed monthly income, may consider government annuities or private immediate annuities.

High-Income Professionals: For taxpayers in higher brackets, QDAPs offer valuable tax deductions during the contribution period while also building up retirement reserves.

Conservative, Low-risk Investors: Those who worry about market volatility and want a more predictable retirement income may resonate with the guaranteed nature of annuity payouts.

Those who are younger, need more liquid assets, or want higher returns may wish to explore more diversified investment options via Longbridge Academy before deciding on annuities for their retirement plan.

How Should Annuities Fit Into Overall Retirement Planning?

Annuities should not be your sole retirement pillar—they are best as the “defensive” component of your asset mix.

Stable Income Layer: Use annuities (government or QDAP) to provide a steady cash flow for essential daily expenses, reducing your exposure to market swings.

MPF Accumulation: Continue managing your MPF wisely, choosing funds that match your risk profile for a lump-sum retirement reserve.

Other Investment Assets: Pursue capital gains and inflation hedges with stocks, ETFs, REITs, and other investment products.

Emergency Reserve: Maintain 6-12 months of cash savings to cover medical or other sudden expenses.

If you want to learn more about global investment options, Longbridge’s market info platform provides real-time data and the latest financial news to help guide your retirement asset allocation.

Frequently Asked Questions

What’s the Difference between Annuities and Savings Insurance?

Annuities are designed to provide “ongoing income distribution”—i.e., regular cash flow. Savings insurance mainly targets “capital accumulation,” paying out a lump sum at maturity. Both are insurance products, but serve different purposes: annuities suit retirees needing a stable income.

Can I Surrender My Annuity Policy?

Generally, annuities can be surrendered, but this usually comes with surrender charges or penalties, meaning you may get back less than your total premiums, especially if surrendering early. Always evaluate your finances to ensure you can commit long term.

How Do I Apply for QDAP Tax Deduction?

When filing your Hong Kong Salaries Tax return, you can claim QDAP premium deductions in Part 10 of the form. Insurers typically provide you with a policy year summary within 40 days after the tax year, listing eligible premiums paid, which you can use to support your deduction claim.

Which Is Better: Government Annuity or Private Annuity?

Each has its pros and cons, suited to different needs. Government annuities are backed by a government entity, with low credit risk and full premium guarantees, making them preferable for retirees and conservative individuals. Private QDAPs are more flexible with application age and offer tax deductions, better for working people planning ahead. They aren’t mutually exclusive—many people hold both.

Is Annuity Income Taxable?

According to current Hong Kong law, annuity income is generally not subject to Salaries Tax, since it’s not employment or self-employment income. Tax depends on individual circumstances: consult a licensed tax adviser for details.

Conclusion

Annuities are an essential “stabilizer” in Hong Kong’s retirement planning landscape. Whether you pick the fully guaranteed government annuity or a QDAP with tax savings and growth potential, the core value is transforming uncertain lifespan into predictable income.

Before choosing an annuity, clarify your retirement goals, financial status, tax needs, and risk tolerance. Annuities are essentially long-term, low-liquidity commitments: be sure you fully understand their terms and risks before you commit.

Most importantly, annuities are only one part of your retirement strategy. Balancing annuities, MPF, and other investment assets will help you build a more complete retirement financial plan.

Which tool to pick depends on your investment objectives, risk tolerance, market outlook, and experience. Whichever you choose, make sure you understand how it works, its risks, and the trading rules involved, and establish a risk management plan suitable to your situation. For more investment knowledge, visit Longbridge Academy or download the Longbridge App.