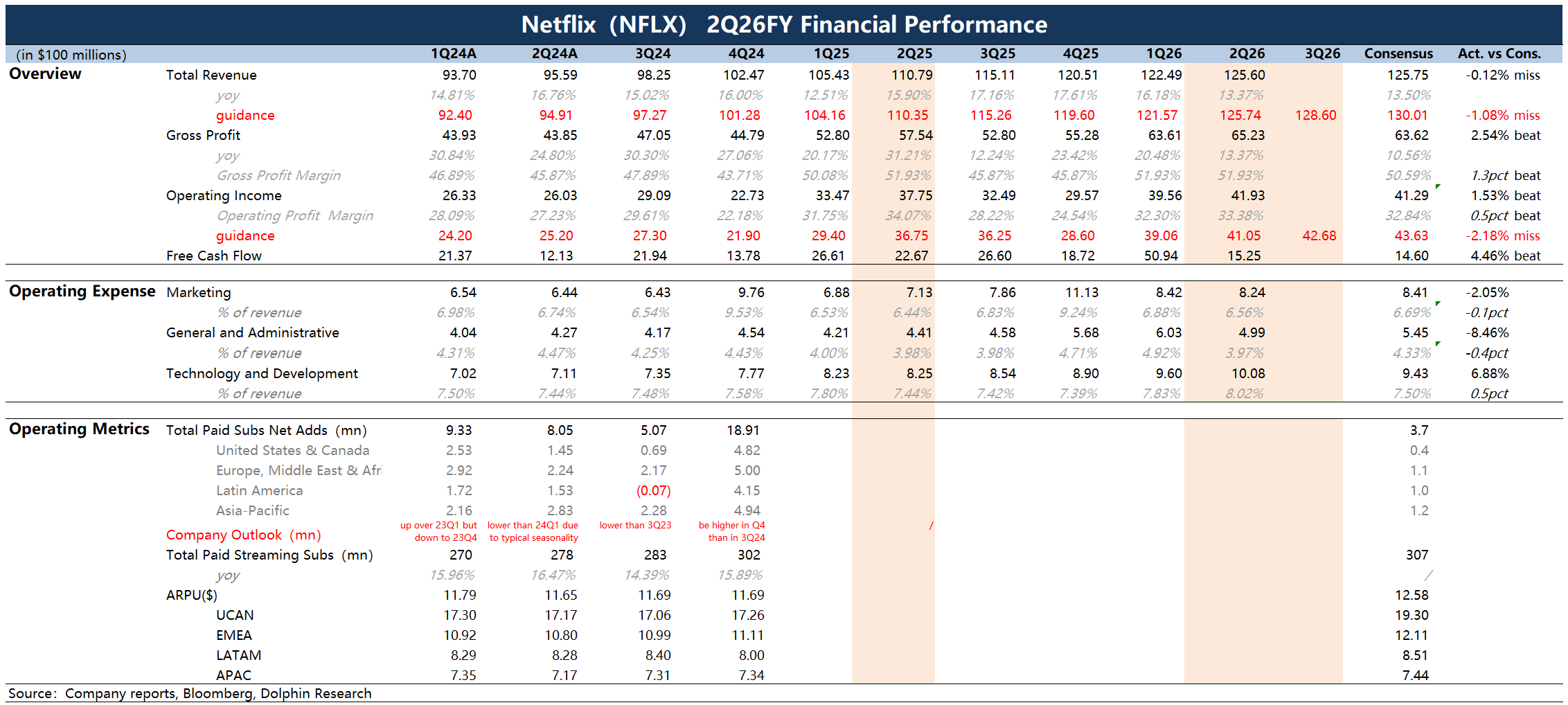

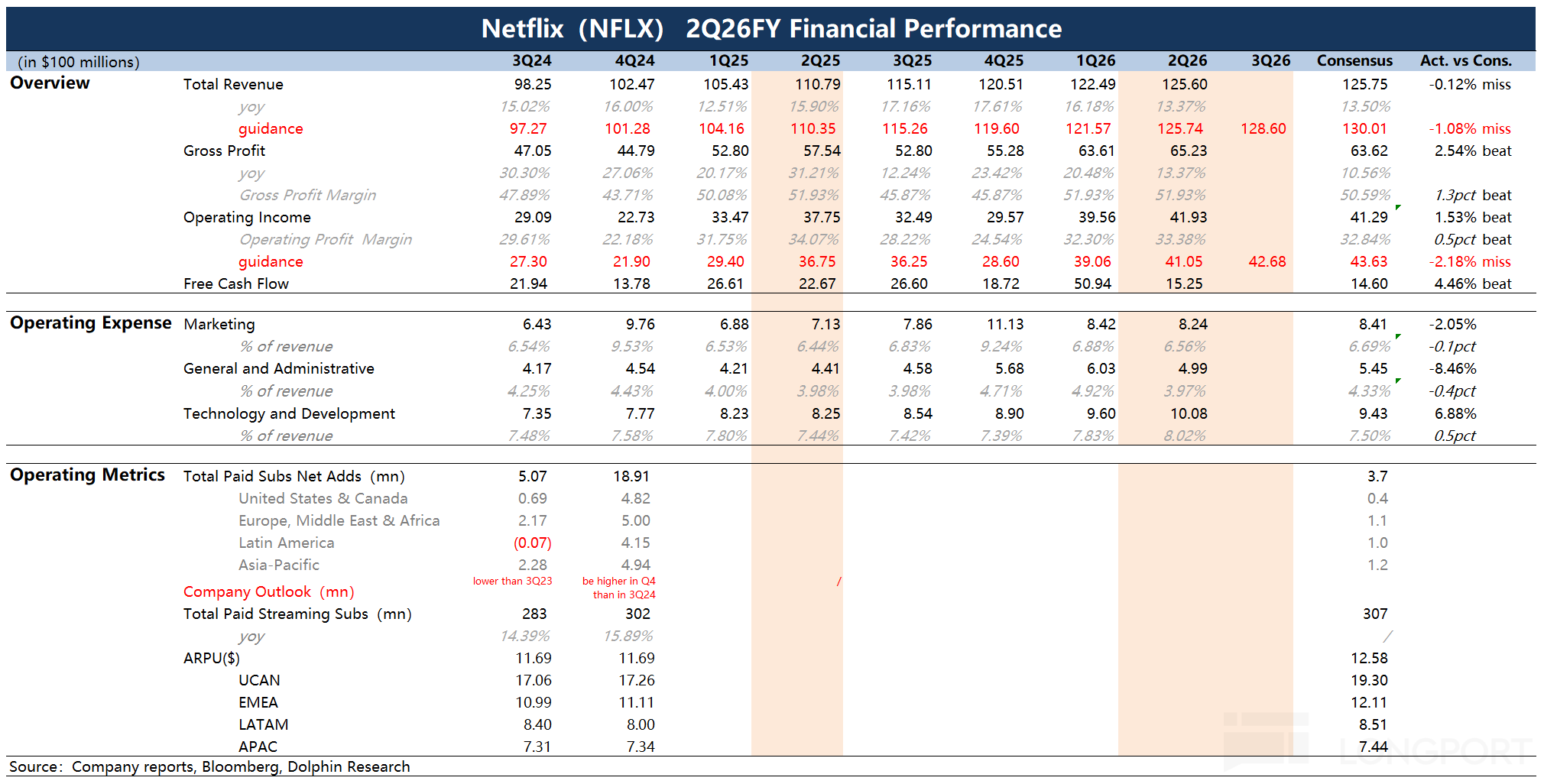

NFLX 2Q26 First Take: Results were lukewarm against modest expectations, with revenue in line with guidance and growth clearly decelerating. The company guided Q3 revenue to $12.86bn, implying further slowdown. NFLX kept its full-year revenue outlook but narrowed the range to $51.0–51.4bn (+13–14% YoY).

Near-term growth softness mainly reflects late-cycle content and the backlash from price hikes in core markets. It also fails to ease investors' medium- to long-term concerns around substitution from short-form video and AI.

The one positive: profitability and cash flow remain relatively stable, even after accounting for a breakup fee on a failed acquisition. This stems from the core business model and potential AI-driven content cost efficiencies.

Beyond that, with the WBD acquisition on hold and a buyback boost announced in Apr., the company repurchased $4.7bn this quarter. This far exceeds its typical quarterly pace in prior years and could continue to help cushion valuation pressure ahead。$Netflix(NFLX.US)