$Oracle(ORCL.US) concentrated profit-taking has created selling pressure. If the stock price pulls back and fills the gap, it will be a good opportunity to add to positions or buy at a low price.

Ginger

GingerSuggestions for you to follow

G

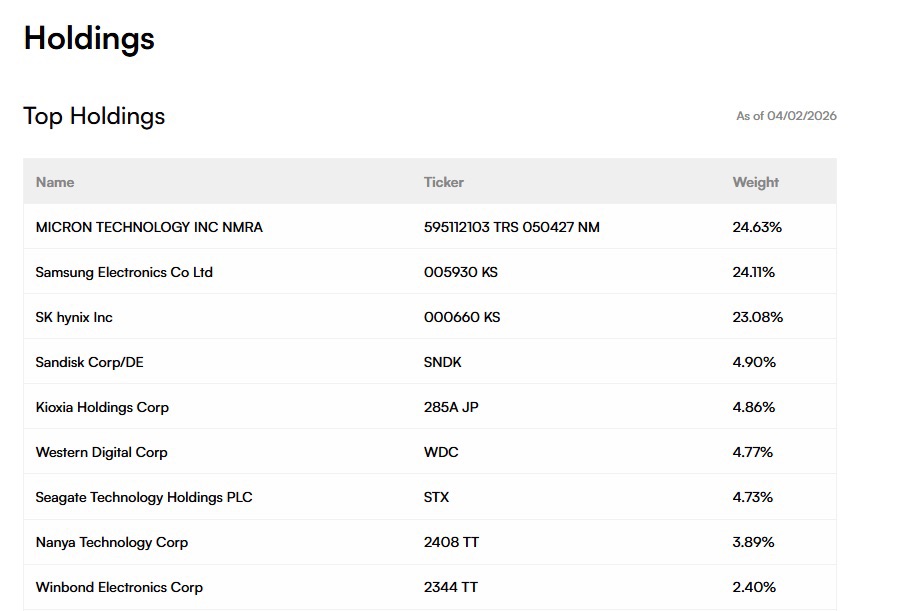

A pure-play ETF focused on the memory sector

1. $Micron Tech(MU.US)- 24.63%

2. Samsung - 24.11%

3. SK Hynix - 23.08%

4. $Sandisk(SNDK.US)- 4.9%

5. Kioxia - 4.86%

6. $Western Digital(WDC.US)- 4.77%

7.$Seagate Tech(STX.US)- 4.73%

7. Nanya - 3.89%

8. Winbond - 2.4%

You can sell ewy and switch to DRAM next week.

G

$Planet Labs(PL.US) announced over the weekend that it will redeem all public warrants, meaning it will uniformly buy back these warrants circulating in the market. Current warrant holders can choose to exercise them and convert them into shares before the end of April.

In the short term, this move will put pressure on the stock price. Because some people may choose to exercise and then sell the shares, or simply cash out, leading to increased selling pressure in the market, which can easily push the price down.

However, from a longer-term perspective, this is actually a positive move. Through this redemption, the company essentially obtains a sum of non-repayable funds, while also streamlining its capital structure. These warrants, which could have triggered selling pressure at any time, are now completely cleared.

Once we pass the end of April deadline and the selling pressure from these warrants is mostly released, the company will have more funds on hand, and the "historical burden" hanging over the stock price will be gone, making the overall situation more favorable.

So it can be understood as:

From now until the end of April, it's more of a phase of short-term pressure, but one that may offer a "discounted buying opportunity."

G

$Applied Optoelectronics(AAOI.US) disclosed that a leading hyperscale cloud provider has placed an order for approximately $53 million worth of 800G single-mode optical transceivers, primarily for AI data center network upgrades. The order is expected to begin delivery in the second quarter of 2026 and be completed by mid-third quarter, subject to final customer certification progress. CEO Thompson Lin stated that the 800G solution can effectively increase network bandwidth, reduce power consumption, and alleviate transmission bottlenecks within data centers amid the rapid expansion of AI computing demand.

Notably, this order closely follows a previous order of approximately $200 million for 1.6T optical modules from the same customer, indicating the customer's continued investment pace in higher-bandwidth solutions. Boosted by this news, the company's stock price rose 9.39% to $95.76 on March 23. Those who didn't enter the market today can wait for a golden cross to appear on the KDJ indicator before entering, or they can sell put options at $80 to earn some premium while waiting to potentially acquire shares.

The consecutive receipt of large orders reflects the accelerated advancement of AI infrastructure construction, significantly driving demand for high-end optical modules. However, equity dilution pressure and intensifying industry competition may also bring risks of significant stock price volatility.

G

$Oracle(ORCL.US) will most likely drop below 150 tomorrow.

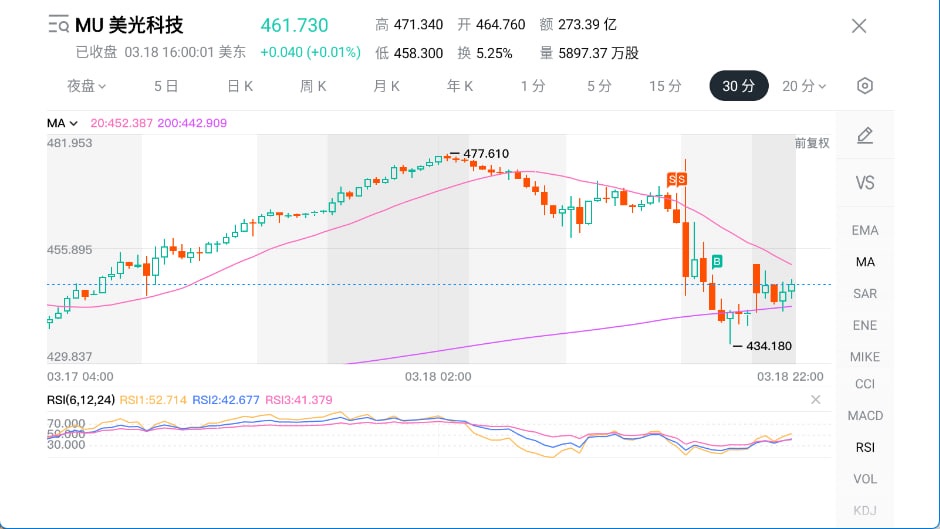

$Micron Tech(MU.US) It's quite a pity after hours, the limit order at 435.01 wasn't filled.

G

$Micron Tech(MU.US) has entered a high-level adjustment phase after completing a large-degree five-wave rise. The current pattern is more likely a WXY corrective structure. It is not advisable to chase the high now, as the stock price has repeatedly hit new highs today, and the Q2 earnings report will be released after the market closes tomorrow.

If the earnings report is positive tomorrow, it is expected to continue rising with a target of 500; if the report is negative, wait for a pullback near the support level before considering entering.

G

$Oklo(OKLO.US) Market manipulation? Short trap? I'm convinced it will definitely rise after the earnings report.

G

The current stock price is near the Fibonacci 78.6% level, and the corrective wave C has also fallen close to this level. After-market earnings report tomorrow, $Oklo(OKLO.US) currently still has zero revenue, but the market is focused on the progress of NRC approval and the fulfillment of Meta's orders. If the news is positive, the stock price may rebound here, currently looking at 84. If the earnings report is negative, then we'll need to find a new bottom.

G

If you still focus on end products like optical modules, you might be overlooking a key but low-key player in the upstream supply chain—$Tower Semicon(TSEM.US). In the silicon photonics and CPO ecosystem, it's more like the core foundry platform supporting underlying manufacturing capabilities.

Why is next week a critical juncture? Because NVIDIA's GTC conference is about to start, and the industry is buzzing about new photonics architectures. In fact, last month NVIDIA openly announced its collaboration with Tower to jointly advance the mass production of 1.6T silicon photonics. This is essentially laying the groundwork for technology and industry expectations ahead of the March launch event. Once downstream manufacturers start accelerating the adoption of related solutions, Tower Semiconductor, as a key silicon photonics foundry platform, is expected to further solidify its position and bargaining power in the supply chain.

Core logic: The growth path is clear and predictable, while market pricing still appears undervalued.

1. Capacity is being snapped up like crazy: 70% of silicon photonics capacity before 2028 has already been pre-booked! What does this mean? The spots are already filled even before the photonics technology truly takes off.

2. Profit expectations are set to soar: Current valuation models probably haven't factored in the "price increase" element. With surging demand, capacity quota premiums are inevitable. Revenue is heading towards $2.8 billion by 2028, and profits are highly likely to exceed expectations.

3. Extremely high certainty: With 70% of capacity already locked in, downside risks are capped. It's a solid "asymmetric" opportunity—limited risk, huge upside potential.

As a key foundry in the upstream supply chain, Tower Semiconductor is a "hidden champion," and its market value hasn't been fully recognized yet. The valuation reflected by the current stock price is clearly low. However, I predict that NVIDIA's GTC launch event will be a significant catalyst triggering the market to reassess the core value of silicon photonics foundries.

Operation: Enter if the stock price pulls back to the support level of 115-112 without breaking it. If it stabilizes above the 20-day moving average with increased volume on the right side, you can enter and look for a move towards previous highs. Those with no position can wait for a pullback (sp).

(Personal opinion, not investment advice)

G

$Intel(INTC.US) rose 2.63% today, and the market is starting to refocus on its potential for further gains. From a fundamental perspective, Intel is not lacking in logic; rather, the relevant logic is still in the process of being gradually realized.

The recent improvement in market sentiment is mainly due to a recovery in data center demand, coupled with growth in AI-related chip and server orders. At the same time, the company's progress in its foundry business and advanced process roadmap has also led some funds to begin positioning early for a "recovery expectation."

However, it will take time for these logics to truly translate into sustained stock price gains. Whether it's improving yields on advanced processes, ramping up shipments of AI chips, or expanding foundry customers, they all ultimately need to be validated by actual revenue and profit growth.

From a trading perspective, the risk-reward ratio for short-term speculation is not particularly high, and the current volatility structure may not be fully over. However, if we extend the time horizon to a 6-12 month mid-term cycle, the current price range, having retreated from previous sentiment highs, actually provides a more comfortable entry point, as the company's fundamental logic has not materially changed.

Looking ahead, if Intel can successfully achieve stable mass production of advanced processes within 2026, while its AI server and data center businesses continue to grow, the market may revalue it closer to a growth tech company rather than a traditional cyclical semiconductor company. If this expectation is gradually fulfilled, it is not impossible for the stock price to reach the $60–70 range by the end of 2026.

From a technical structure perspective, the area around 50 is a key resistance zone. Once the price effectively breaks through this range with volume support, it is expected to further challenge and break through previous highs, opening up new upside potential.

In the short term, the stock price is more likely to consolidate within the $44–51 range, digesting holdings and overhead pressure through sideways movement, waiting for further catalysts from fundamentals or news to drive a breakout to new highs for the phase.

G

Recently, the market has engaged in extensive discussions about $Hims & Hers Health(HIMS.US). The primary reasons are the uncertainties surrounding its weight-loss drug business, regulatory environment, and partnership with pharmaceutical giants, leading to significant stock price volatility. Some institutions hold a pessimistic outlook on HIMS and have adopted large-scale short-selling strategies, citing reasons such as potential zero future revenue growth and risks of financial and operational pressure from FDA and Novo Nordisk-related lawsuits.

However, the plot took a clear turn last Friday. Novo Nordisk announced it will sell its weight-loss drug products on the Hims platform, and both parties have ended the dispute that escalated to legal action last month. This move establishes a legitimate global distribution network, keeps Hims' balance sheet healthy, and forms a strategic partnership with a major pharmaceutical company. Against this backdrop, there remains a significant amount of uncovered short interest in the market.

Following the announcement, Hims' stock price rose nearly 40% in after-hours trading. When the market opens next Monday, the stock price is expected to continue its upward trend. If short sellers begin large-scale stop-loss covering, a rapid price surge could occur in the short term. Of course, another possibility exists: as the partnership with Novo Nordisk progresses, Hims' fundamentals gradually improve, and the short squeeze will proceed at a relatively slower pace, with the stock price rising steadily.

When the market opens next week, I will do my part to turn the shorts into fuel sooner. However, for stability, it's still advisable to wait 30 minutes to an hour after the opening, observe the market turnover rate and trading volume to gauge the strength of the short covering before deciding whether to enter. In the current geopolitical environment, the impact of the broader market cannot be ruled out.

G

An Undervalued AI Company - Amazon

Many people still habitually think of $Amazon(AMZN.US) as an e-commerce company, but I believe it is rapidly transforming into an AI infrastructure company. First growth curve: The wave of large models With the explosive growth of large model applications, computing power demand is rising exponentially, and AWS remains one of the world's core cloud infrastructures. Whether it's model training, inference, or AI application deployment, a massive amount of workload ultimately relies on cloud platforms. This means that each round of AI expansion will directly drive demand and revenue growth for AWS...

G

What should we start buying in the US stock market next week?

The US and Iran are at war, what to buy when the market opens next week? Almost everyone is saying: buy oil, buy gold, buy defense stocks. But no one tells you: hedge funds' net long positions in crude oil are at a 22-month high, gold has risen for 7 consecutive months, reaching a historical high of $5,278, and the defense sector has already risen 17% to 34% year-to-date. Smart money had already positioned itself before Friday. The price you can buy at Monday's open is the price they are willing to sell to you. In 2020, when the US killed Soleimani, oil prices jumped 4% on the first day, only to give back all gains within a week. In June 2025, when Israel struck Iran's nuclear facilities, oil prices rose over 12%...

G

Jensen Huang proclaims "Inference is revenue," and NVIDIA's computing power hegemony is just beginning.

NVIDIA has delivered another record-breaking earnings report.

After the US stock market closed on February 25th, NVIDIA announced its latest quarterly revenue reached $68 billion and provided strong guidance. However, in a dramatic turn, the stock price surged over 4% after the earnings release but turned negative following the conference call. The market's hesitation precisely exposes the greatest divergence regarding the future of AI.

And during the conference call, the remarks from NVIDIA CEO Jensen Huang might be the signal truly worth pondering repeatedly.

He said: "The inflection point for Agentic AI has arrived."

What is Agentic AI? It's not the ChatGPT that chats with you, nor is it the Midjourney that draws pictures. It's AI capable of autonomous decision-making and task execution—a true "digital employee." When companies begin deploying these digital employees on a large scale, they need to generate massive amounts of Tokens, and behind every Token is computing power being consumed.

Jensen Huang's logic is extremely clear and also extremely cold: without computing power, you cannot generate Tokens; without Tokens, you cannot achieve revenue growth. The massive capital expenditures that cloud service providers are pouring in today will ultimately be directly converted into revenue.

In other words, computing power is no longer a cost, but the fuel for the money-printing machine.

He added another point: "The current space data center economy is still barren." In Jensen Huang's eyes, today's AI infrastructure is like the early Wild West—desolate, empty, and no one knows how to make money. But he is certain that the situation will change, and it is changing.

Most notably, NVIDIA confirmed it is close to finalizing a massive infrastructure cooperation deal with OpenAI, with order demand already scheduled into 2027. The GPUs you cannot buy today have already been pre-ordered for three years later.

Jensen Huang had actually given the answer long ago. Last year, he said something that was considered mere rhetoric at the time, but looking back now, it was prophetic: "We are creating a new means of production, called computing power." Not a tool, but a means of production. Whoever controls computing power controls the power of distribution.

Wall Street is now divided into two camps. One believes AI is a bubble, and capital expenditure is unsustainable; the other believes AI is infrastructure, and we are only in the very earliest stages of its construction. Jensen Huang is clearly in the latter camp. He compares data centers to "barren space," meaning: you think it's desolate because you haven't yet seen what can be grown in space.

If in the future every enterprise needs its own digital employees, and if every digital employee needs to consume massive amounts of Tokens daily, then NVIDIA selling the shovels, the cloud providers mining for gold, the enterprises using AI, and even every ordinary person will be swept into this transformation.

Jensen Huang had another statement that, looking back today, might be the most accurate prophecy: "We're not selling chips, we're building time machines."

Computing power is the ticket to the future. Some are still hesitating whether to buy a ticket, while others have already taken a seat in the cockpit.

G

NVIDIA's earnings report is explosive, but its stock price has slumped.

Let's break down NVIDIA's financial report in detail. NVIDIA's revenue and profit have once again reached record highs. Total quarterly revenue: reached a record $68.1 billion, up 20% quarter-on-quarter and a significant 73% year-on-year. Diluted earnings per share were $1.62, significantly exceeding analysts' previous expectation of about $1.53. Net profit for the single quarter reached approximately $43 billion, almost doubling year-on-year. The data center business remains the "strongest engine." Data center revenue: Q4 recorded a record $62.3 billion, up 22% quarter-on-quarter and 75% year-on-year...

G

To be honest, the reason I was able to hold onto stocks that doubled this year wasn't by predicting the macro environment or through god-like stock picking. It was by understanding these eight words: Choose the right track, follow the logic. Many people are betting on a reversal or an emotional bottom, while smart money is always asking the same question: Where is the next "physical bottleneck" in AI expansion?

Money will only pile up where there's a "choke point." Below are the four major "bottleneck assets" I've identified after reviewing this year's return curve:

1️⃣ Memory – The Fuel for Computing Power

📍 Targets: $Micron Tech(MU.US), $Sandisk(SNDK.US), $Silicon Motion Tech(SIMO.US)

No matter how powerful the computing power is, if the memory can't keep up, the system will freeze. HBM, DRAM, NAND are no longer optional; they are necessities. This is the bottleneck premium.

2️⃣ Photonics – The Achilles' Heel for Eliminating Latency

📍 Targets: $Lumentum(LITE.US), $Coherent Corp.(COHR.US), $Applied Optoelectronics(AAOI.US), $AXT(AXTI.US)

When data centers expand to the GW level, even the strongest GPUs are useless if the connection speed can't keep up. Optical interconnect is the lifeline of AI infrastructure.

3️⃣ Power/Grid (Utilities) – Energy is the Foundation

📍 Target: $XLU (Utilities ETF)

The ultimate limit of AI is energy! Data centers are power-hungry monsters. With every round of computing power expansion, the power grid is a passive beneficiary. This is a digital revolution, and even more so, an energy revolution. ⚡️

4️⃣ Advanced Packaging (Capex) – The Last Mile of Implementation

📍 Targets: $Amkor Tech(AMKR.US), $Onto Innovation(ONTO.US), $Camtek(CAMT.US), $Kulicke and Soffa(KLIC.US)

Everyone is watching NVIDIA, but the real production bottleneck is the packaging stage. HBM, Chiplet, and advanced packaging are the true choke points for implementing computing power.

💡 The most important lesson learned this year:

Don't try to be a "reverse savior"! Don't be obsessed with betting on a SaaS recovery or a cybersecurity rebound.

Following liquidity is more important than trying to be clever. When demand explodes, bottleneck assets have inherent pricing power. Keep asking: Where is the next place that will get stuck? Getting in before everyone else sees it clearly is the key to widening the performance gap. 🚀

G

Currently, $Intel(INTC.US) has reached the seventh bar of the low-nine structure on the daily K-chart. Regardless of whether this low-nine signal ultimately proves valid, it is recommended to observe more and act less at this stage. Looking at the weekly K-chart, the golden retracement shows support near 42.5. First, see if this level holds as effective support. Secondly, pay attention to the MA100 moving average. If this level is breached, then cut losses and exit immediately to prevent the trend from deteriorating completely.

G

HSBC raised PLTR's target price to $205

When Wall Street starts chasing prices, I'm more concerned about how far this growth curve can go. When HSBC upgraded $Palantir Tech(PLTR.US) from "Hold" to "Buy" and raised the target price from $197 to $205, it seemed like just a minor adjustment on the surface. But what's really worth dissecting is the growth structure behind its core. The performance of the U.S. commercial segment is the reason for this upgrade. In this model, contract backlog determines future revenue visibility. However, there's also a point worth noting in the report. HSBC mentioned...

G

The US military budget for 2026 is close to $1 trillion. Although it increased by 13% year-on-year, the most explosive part is not the total amount, but where the money is going: heavy assets are giving way to "algorithms + unmanned swarms"!

The future battlefield will no longer be a contest of pilots, but a duel of AI computing power.

I've compiled a list of 6 representative companies in this wave of "military intelligence" (not a recommendation, just a logical breakdown):

Unmanned Aerial Vehicle (UAV) direction:

1、$Aerovironment(AVAV.US): The maker of the "Switchblade" drone with an impressive track record. It has relatively high order certainty and holds billions of dollars in contracts.

2、$Red Cat(RCAT.US): Focuses on small military drones, already integrated into the US military system. If orders continue to grow, it's a long-term business.

3、$Kratos Defense & Security(KTOS.US): Works on unmanned combat aircraft and hypersonic-related technologies. High potential, but the key is whether the military will make large-scale purchases later.

AI Hub and Computing Power

4、$Palantir Tech(PLTR.US): The "brain" of the future battlefield. It doesn't build aircraft, it builds command systems that link drone swarms into a collaborative network.

5、$One Stop(OSS.US): Edge computing hardware, enabling unmanned vehicles to possess formidable computing power even without network connectivity.

Dark Horse Potential, Small-Cap Volatility Stocks

6、$Ondas(ONDS.US): Small size, high elasticity. The core logic is its autonomous control system. The next step is to see if it can meet the 2026 revenue guidance of $180 million!

A word of caution:

Defense stocks are different from tech stocks. They have long order cycles and are heavily influenced by policy, especially small-cap companies which experience very volatile swings—they surge fiercely and fall just as unceremoniously.

Summary:

The nature of warfare has changed! It has shifted from "expensive, few, large equipment" to "cheap, numerous, autonomously collaborative unmanned swarms." Whoever can best integrate "unmanned systems + AI + computing power" will likely be the core beneficiary of the next phase of military upgrades.

G

$Intel(INTC.US) A TD Sequential low nine signal has appeared on the weekly chart. Combined with the current price structure analysis, it is highly unlikely that this week's closing price (today's close) will effectively break below $46.9, which can be considered a temporary defensive level.

The daily chart shows that the price is still operating within an upward channel, currently above the support zone at the lower channel boundary of $45.6–$46. If this support fails, attention should turn to the secondary support band in the $42–$43.5 range below.

Key resistance above is concentrated in the $50–$51.5 area. If there is a high-volume effective breakout above this range, it could potentially challenge and break through the previous high, opening up further upside space.

Overall, the current structure leans more towards consolidation within the $47–$51 range, digesting supply and pressure through sideways accumulation, waiting for fundamental or news catalysts to cooperate, thereby driving the price upward to break through and set a new stage high.

G

Is Robinhood's earnings report a surge or a bomb?

Robinhood (HOOD) will announce its Q4 and full-year 2025 earnings after the market closes today. From the "retail investor stronghold" of the past to the current "all-in-one financial platform," tonight's report is of extremely high quality! As an investor, these four key points determine whether HOOD can continue to soar: 1. Business Diversification: Breaking free from "relying on market conditions"? In the past, Robinhood heavily depended on trading revenue driven by market volatility. But now it has transformed: the Gold subscription service continues to hit new highs, and this kind of stable cash flow is exactly what the capital market loves...

G

What's the outlook for US stocks next week? Are tech stocks out of favor? These sectors are quietly rising!

The major indices ($SPDR S&P 500(SPY.US) /$Invesco QQQ Trust(QQQ.US) ) are looking a bit downcast because the tech giants have been performing flat. However, small-cap stocks and equal-weighted indices ($iShares Russell 2000(IWM.US) /$Invesco S&P 500 Eq Wgt ETF(RSP.US) ) are quietly hitting new all-time highs! This means: Big Tech is taking a break...

G

JPMorgan upgrades to "overweight", analysis of sofi's fundamental + technical resonance

$SoFi Tech(SOFI.US) JPMorgan analyst Reginal Smith upgraded SoFi's investment rating from "Neutral" to "Overweight" on Tuesday, maintaining a $31 target price. At the current stock price, this target implies roughly 40% upside potential. Across the fintech sector, conditions remain chilly, with many companies facing pressure from layoffs, losses, and even business contraction. But SoFi has clearly bucked the trend, with not only continued user growth but also rapid deposit expansion...

G

Can PLTR still be chased? Must think clearly about these three things before the earnings report

Can Palantir still be chased? Must think clearly about these 3 things before earnings report: Many people have been watching Palantir (PLTR) recently, but do you really understand it? It's not a new AI company. Palantir has been around for 23 years, initially focusing on government data analysis, and only went public in recent years. The real growth driver: AIP The current growth core comes from AIP (Artificial Intelligence Platform): Enterprises can quickly apply AI to their real business operations, which directly drives explosive growth in commercial clients. How strong is the stock price? In the past three years...