SanDisk (Sandisk / SNDK related assets) — The "ammunition depot" behind AI 💾

If you're bullish on AI but find NVDA too expensive, storage is the second line

Why recommend

AI's demand for storage is "the most essential of essentials"

Training, inference, data centers

Computing power can expand, but storage must keep up

Enterprise SSD and data center storage demand has clearly recovered

The storage industry is in the recovery phase from the bottom of the cycle

The past 1–2 years have been a price hell

Now:

👉 Production cuts completed

👉 Inventory declining

👉 Prices starting to rebound

The most comfortable position for cyclical stocks: just emerging from the bottom

SanDisk is a "high-purity" storage play

No flashy stories

It’s all about price recovery + demand revival

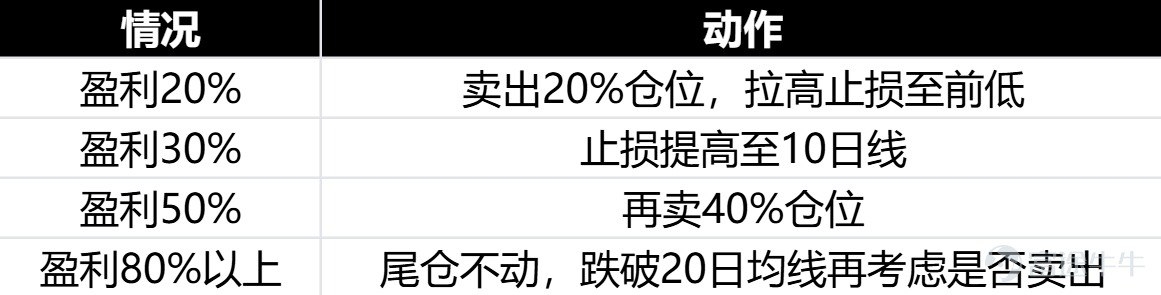

Risks & Notes

More volatile than Apple

Belongs to cyclical elastic stocks

Who it suits

Bullish on AI infrastructure

Can tolerate some volatility

Wants to ride the industry recovery elasticity

3. Intel (INTC) — A "hated by the market but with extremely high odds" turnaround play 🧠

Intel isn’t a "good student," but it could be a good reversal

Why recommend

Valuation is truly low

Compared to other semiconductor giants, Intel:

Lower market cap

Lower expectations

Lower positioning

👉 Once it’s "not as bad," the stock has room to rise

The banner of U.S. semiconductor independence

Clear policy support (manufacturing reshoring)

Chip foundry is a long-term strategy

May not win immediately, but unlikely to die

AI isn’t the main act, but there’s a catch-up logic

The market doesn’t expect it to beat NVDA

Just needs to: Stabilize server CPUs

Make progress in foundry

👉 Valuation will be repriced

Risks matter (truth)

Execution has always been questioned

Pressure to catch up technologically

👉 This isn’t certainty, it’s about odds

Who it suits

Can accept slow, grinding, repeated moves

Wants to bet on reversal + valuation repair

Position sizing shouldn’t be too heavy

SanDisk: AI elasticity, cyclical rebound, recovery

Intel: High-odds reversal, valuation repair

👉 Not betting on the same logic

👉 It’s a "stable + elastic + gamble" structure

SanDisk: If AI doesn’t stop, data won’t stop, and it’ll keep eating

Intel: When no one loves it, the odds are actually the best

Personal opinion, not investment advice