$Alphabet - C(GOOG.US) -3% AH after missing on 2Q non-GAAP earnings and boosting its FY’26 CapExp, potentially triggering a new CapExp arms race.

$Alphabet - C(GOOG.US) now projects a 2026 CapEx range of $195B to $205B, up $15B from its prior guidance, which the company says is necessary to meet the demands of the AI infrastructure boom. Many analysts were expecting GOOG to lift its CapEx outlook, after Google announced an $85 billion equity raise last month. The higher guidance reflects the company’s efforts to accelerate its expansion of AI computing capacity and book more revenue from cloud-computing clients. Still, the negative free cash flow and heavy bill for AI infrastructure is fueling investor jitters.$Alphabet - C(GOOG.US) 2Q cloud revenue totaled $24.8B, up +82% from a year ago and above the $22.5B analysts had expected. The company’s cloud backlog, a measure of contracted work that hasn’t yet been recorded as revenue, grew to $514B, up from roughly $460B, a quarter earlier.At a 2026 P/E of 23.6x and +15% forward long-term rev growth and +17% forward long-term eps growth, $Alphabet - C(GOOG.US) still looks compelling and should be bought on weakness.

Gary Black Tracker

Daily quotes, trades and insights from Gary Black.

Gary Black TrackerSuggestions for you to follow

G

$Tesla(TSLA.US) (-3% AH) after missing on auto gross margins ex-reg credits (16.3% vs 18.4%) which drove huge miss in non-gaap eps ($.33 vs $.55 WS est). CapExp of $5.8B caused free cash flow to go negative -$1.1B, which was expected. On the positive side, active FSD subs of 1.48M was 16% QoQ vs 1Q (+63% annualized) and the 2Q attachement rate of FSD to North American deliveries was a record 55%. Optimus production is still scheduled to begin late-2026.

Conf call at 530ET. Investors most want to hear how quickly unsupervised autonomy without safety monitors (currently 40 TSLA vehicles vs Waymo 3,500 vehicles) can scale.

G

I asked Grok if there has ever been a company in the history of the stock market like $SpaceX(SPCX.US) with more than $1 trillion market cap that traded for over 40x forward EV/Rev?

Grok’s response: No, there has never been a company with a sustained >$1 trillion market cap trading at over 40x forward EV/Revenue. $SpaceX(SPCX.US) stock is in uncharted territory and will likely continue to decline under the weight of its extreme valuation. $NVIDIA(NVDA.US) was the closest candidate but even it falls short on forward EV/Rev multiple above 40x at a trillion-dollar scale.• NVDA first hit ~$1T market cap in May 2023 and has since reached $4T–$5T+.• Trailing EV/Rev peaked at ~44.9x historically. • Forward (NTM) EV/Rev has been significantly lower, typically in the 10–25x range during its $1T+ period, reflecting aggressive revenue growth forecasts (often 50%+ YoY in data center/AI). Recent valuations hover around 11–13x forward revenues in analyst models.High forward EV/Revenue multiples (>40x) would imply extreme optimism not supported by consensus estimates even at Nvidia’s peak hype. Its forward P/E has exceeded 40x at times, but revenue multiples compress faster due to scaling sales.

G

Don’t say I didn’t warn you.

$SpaceX(SPCX.US) now sits at $126/share - a stunning 45% reversal in just one month from its post-IPO peak of $226 and well below its IPO price of $135. SPCX still trades at FY’2026 EV/Revs of 45x. Source: Financial ReviewIconic Wall Street investor Peter Lynch was not a fan of buying into small IPO floats, and liked to say that IPO stood for “it’s probably overpriced”.The totally unproven plans to build data centres in space were endlessly dissected. The SPCX prospectus spelled out the ridiculous total addressable market the company was claiming: $US28.5 trillion, close to the entire GDP of the United States. SpaceX’s losses were disclosed and discussed.Indeed, there may not have been an IPO in world history as closely scrutinised as this one. If investors still wanted to buy in despite all the risks, they deserved what they got.That’s fair enough, at one level, but it ignores the cynical way that SpaceX, its investment bankers and its advisors structured this IPO to engineer short-term gain – and a $US500 billion fee pool – with seemingly little concern for long-term investors.As Schroders head of Australian equity Martin Conlon wrote this week, investment banks know that “the vast pools of money directed towards rules-based investment processes”, such as passive investing and algorithmic trading, have changed the way markets work.And so they successfully lobbied index market operators such as Nasdaq and FTSE Russell to – in the words of Conlon – pervert and game the rules so that large, loss-making companies such as SpaceX could gain almost immediate inclusion in major sharemarket indices.The SPCX bankers successfully lobbied index market operators such as Nasdaq and FTSE Russell to game the rules so that large, loss-making companies such as SpaceX could gain almost immediate inclusion in major sharemarket indices.The SpaceX float raised a historic $US85 billion in its IPO - 3x the size of the next largest IPO in history. But the bankers knew that they could create a “highly imbalanced supply/demand situation, where a free float of less than $US100 billion would set the price for more than $US2 trillion in paper market value.Here we are today and SPCX still looks ridiculously overvalued at 45x 2026 EV/Revs. Yet 80% of the 36 WS analysts who have initiated coverage of SPCX have buy ratings on the stock. And only one - Morningstar, which presumably can’t earn future banking fees on SPCX - has a sell rating. That says it all.

G

$Netflix(NFLX.US) -7.7% AH after posting 2Q results in line with consensus but offering 3Q and FY’26 guidance that missed expectations. Mgmt is blaming the 2026 Winter Olympics and World Cup for its misses but investors will continue to focus on NFLX’ lack of new content.

2Q results:- Revs $12.56B vs $12.58B est- Adj EPS $.80 vs $.79 est- Operating income $4.19B vs $4.13B est- Operating margin 33.4% vs 33.0% est3Q guidance:- Revs $12.86B vs. $13.0B est- Adj EPS $.82 vs $.84 est- Operating income $4.27B vs $4.36B estFY’26 guidance:- Revs $51.0B-$51.4B vs $50.7B-$51.7B prior ($51.4B est)- FY rev growth 13-14% vs 12-14% prior- Advertising rev unch’d at $3B NFLX mgmt will likely try to get investors to focus on 2026/1H hours viewed (+2% vs +1.5% in 2025/1H) but to me this level of unit growth is unimpressive. That said, if the company can deliver +10-12% long-term rev growth and +15-17% long-term eps growth (consensus), it looks cheap at 19.4x 2026 Adj EPS.

G

$Netflix(NFLX.US) -7.7% AH after posting 2Q results in line with consensus but offering 3Q and FY’26 guidance that missed expectations. Mgmt is blaming the 2026 Winter Olympics and World Cup for its misses but investors will continue to focus on NFLX lack of new content.

2Q results:- Revs $12.56B vs $12.58B est- Adj EPS $.80 vs $.79 est- Operating income $4.19B vs $4.13B est- Operating margin 33.4% vs 33.0% est3Q guidance:- Revs $12.86B vs. $13.0B est- Adj EPS $.82 vs $.84 est- Operating income $4.27B vs $4.36B estFY’26 guidance:- Revs $51.0B-$51.4B vs $50.7B-$51.7B prior ($51.4B est)- FY rev growth 13-14% vs 12-14% prior- Advertising rev unch’d at $3BG

Still not sure what people see in $SpaceX(SPCX.US) as an investment. It’s already a megacap ($1.8T market cap) so upside is limited. It won’t generate profits until 2027. It trades at 2026 EV/Rev of 47x ( $Tesla(TSLA.US) 14x), and 2026 EV/EBITDA of 110x ( $Tesla(TSLA.US) 97x). I get the new TAM story once other airlines follow Frontier’s lead in adapting SpaceX Starlink as the standard WiFi package on commercial airlines. But 20% of SPCX shares unlock for sale in August and 44% of shares unlock by early September, which would balloon the tradable float by roughly 900%. Valuation has to matter at some point.

G

$Lucid(LCID.US) plunged -45% to $2.98 after an electric-vehicle newsletter (

G

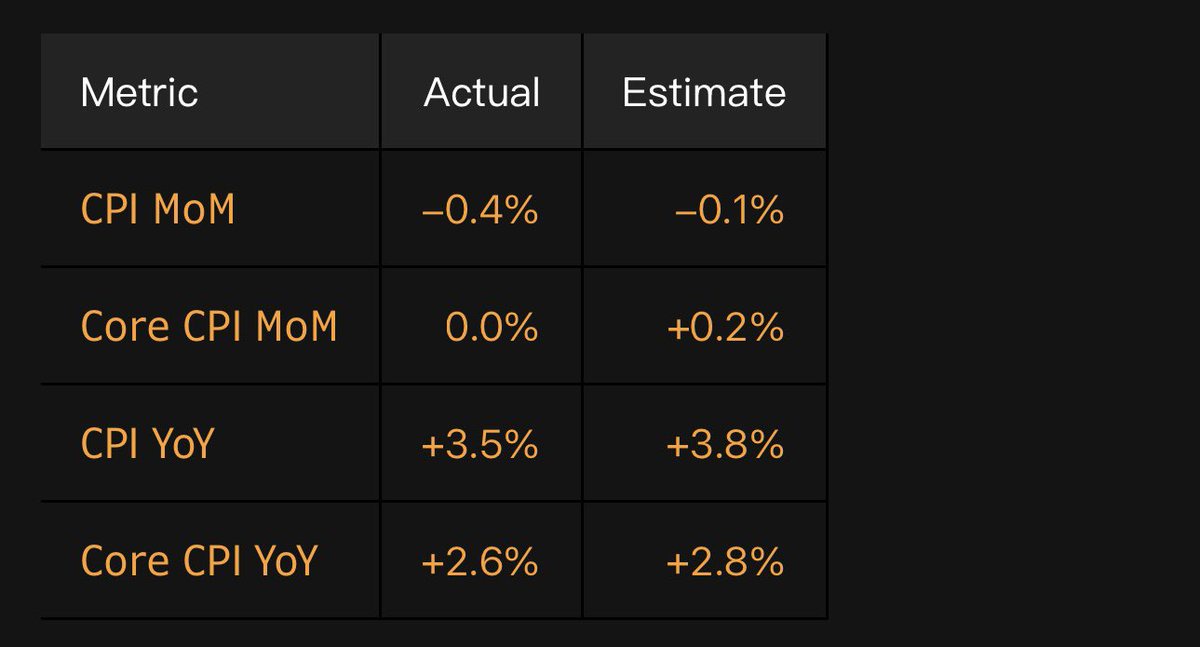

June U.S. CPI came in much weaker than expected in June, including the first month over month decline in six years, taking some pressure off new Fed Chair Kevin Warsh to raise interest rates.

G

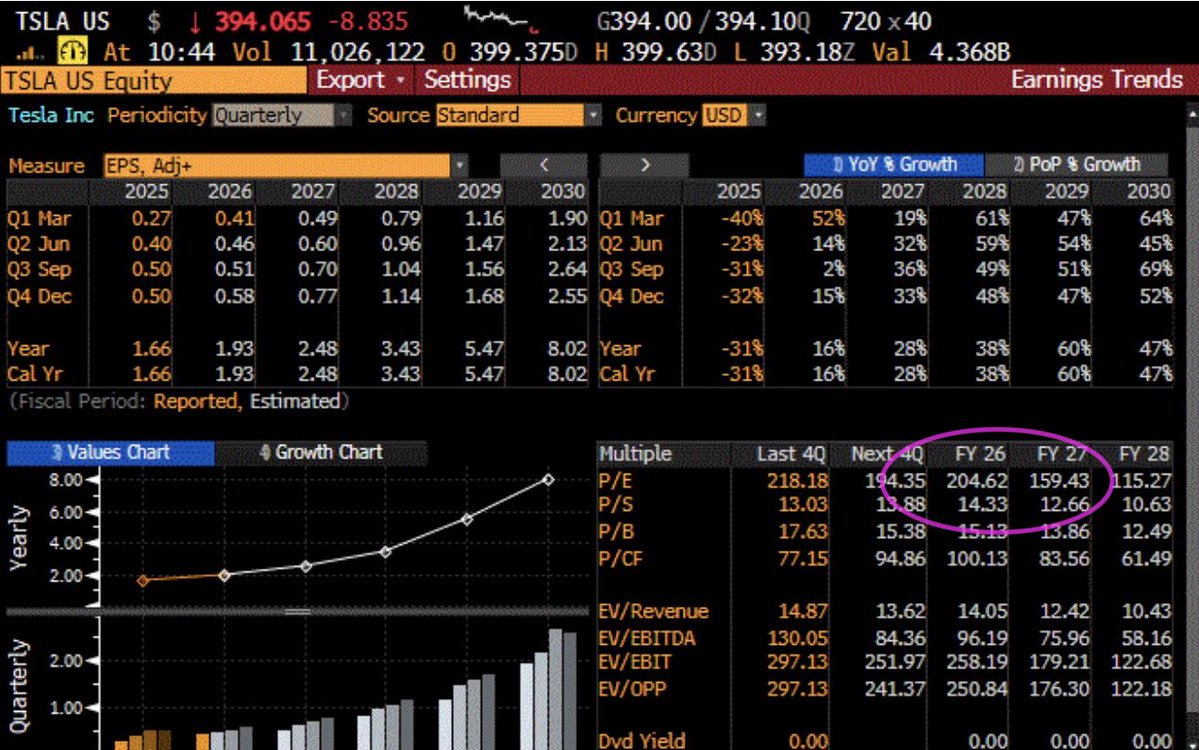

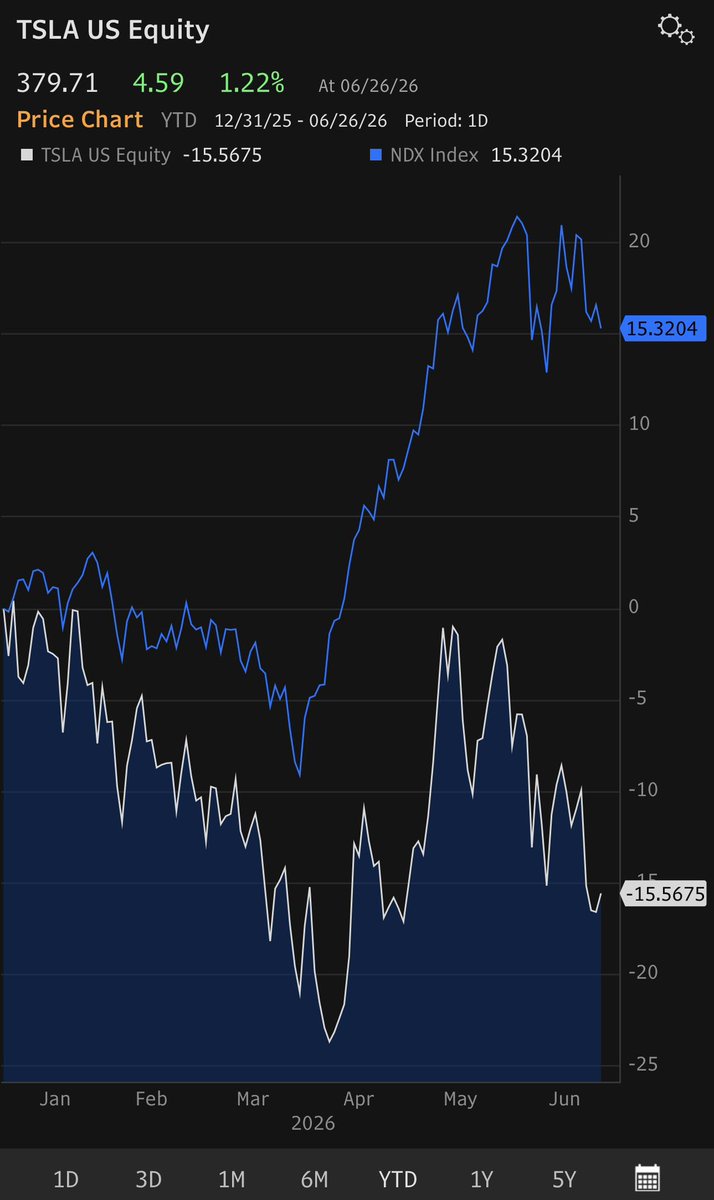

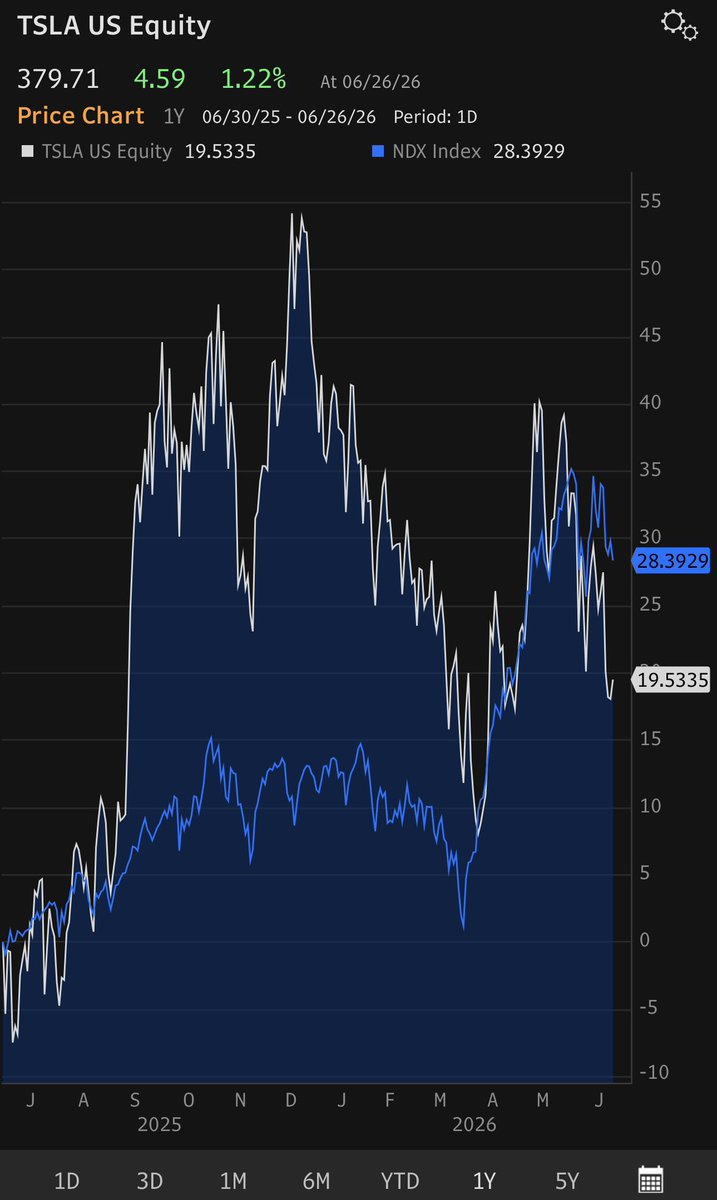

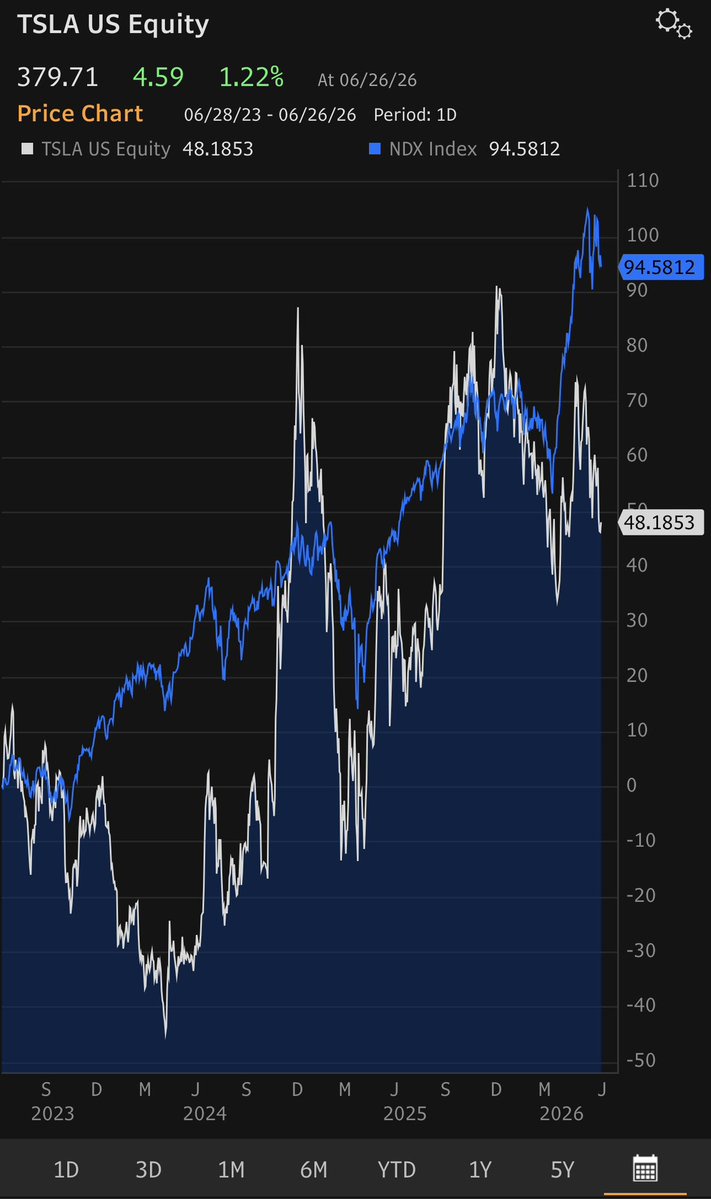

As much as I love $Tesla(TSLA.US) the company, it’s difficult to support the valuation (2026 P/E 209x vs +35% long-term EPS growth, 6x PEG), which remains excessive vs every other Mag 8 name (avg 2x PEG). Most TSLA promoters on X choose to ignore valuation in any discussion of $Tesla(TSLA.US) as unsupervised autonomy becomes commoditized, which is why $Tesla(TSLA.US) continues to underperform YTD (TSLA -7% vs NDX +18%). Meanwhile $SpaceX(SPCX.US) will likely soon fall below its $135 IPO price as 20% of locked shares become free in early-August.

G

$Tesla(TSLA.US) ‘s stretched valuation (2026 P/E of 205x vs 2026-2030 eps growth of +35%, PEG 6.0x) and declining forward earnings estimates (2027 EPS est -17% YTD) are why most institutional investors avoid the stock. Everyone recognizes the unique technological advantages TSLA FSD has, but most X influencers won’t talk about valuation or why analysts’ estimates keep falling. These two reasons (valuation and negative revisions) are why $Tesla(TSLA.US) continues to underperform NDX.

G

Famed investor Jeremy Grantham says history will end up laughing at $SpaceX(SPCX.US), the ‘craziest IPO in the history of man’ that just joined the Nasdaq 100

Summary by Bloomberg AI▪Jeremy Grantham says history will end up laughing at SpaceX, calling it the "craziest IPO in the history of man".▪Grantham is unimpressed by SpaceX's goal to "build the systems and technologies necessary to make life multiplanetary" and thinks its prospectus will be laughable to investors of the future.▪Despite Grantham's skepticism, Wall Street is split on how high SpaceX can fly, with some analysts setting price targets at $300, $205, and $225, and generally agreeing it will soar.By Eleanor Pringle07/08/2026 07:25:45 [FOT](FORTUNE)With Elon Musk’s SpaceX now embedded in the Nasdaq 100, the prospects of the rocket company have–directly or indirectly–now slipped into the stock portfolios of millions of people around the globe.But joining the Nasdaq index has done little to convince critics, who are dubious about the lofty aims of the company. In the prospectus ahead of its offering, SpaceX said its goal is “to build the systems and technologies necessary to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars.”Such statements will be laughable to investors of the future, says Jeremy Grantham, co-founder of investment giant GMO. Admittedly, the billionaire British investor is known for his skepticism: He’s a self-professed “permabear” and has warned AI’s impact will result in “blood in the streets.”It is perhaps no surprise, then, that he is unimpressed by the (literally) out-of-this-world intentions of SpaceX. “Everyone’s lining up to tell you to buy the craziest IPO in the history of man,” Grantham told Morningstar’s The Long View podcast in an episode released this morning, “In 50 years, they’ll be telling and writing stories about SpaceX, and they’ll be quoting you paragraphs from the prospectus, and you will be laughing at it.”Even the most bullish of investors might be feeling a reality check since SpaceX launched. At the time of writing, SpaceX is down 7% over the past month, hovering at around $150 a share—only slightly ahead of the $135 it targeted at launch.Wall Street is split on how high SpaceX can fly, though they generally agree it will soar: Morgan Stanley, for example, has reportedly set the price target at $300, while Goldman Sachs’s Eric Sheridan and team wrote in a note seen by Fortune that they see it closer to $205.Sentiments among analysts are, generally, positive. J.P. Morgan wrote that its target is $225 , adding it believes Elon Musk’s goal of reaching $1 trillion of revenue by 2031 is possible “but requires strong execution across an ambitious timeline.”The note authored by Doug Anmuth, Seth Seifman, Sebastiano Petti, and Richard Choe highlighted some concerns, one of them being the fact that there’s “only one Elon.” They wrote that Musk’s “outsized influence and control (82% voting power) is central to SpaceX’s culture, vision, and operational strategy, and we believe his leadership has been a defining driver of the company’s success. At the same time, that concentration of control raises governance considerations and exposes the company to leadership-transition risk.”Grantham said he was baffled by Wall Street banks’ recommendations to buy SpaceX for their clients. He added: “In the end, the reality will come out, and this will turn out to be, of course, one of the landmark historical events that I so value in history looking back. It will be amazing, by the way, if it doesn’t collapse, because it will need such massive developments on AI that our entire lives are totally different.”Even if the justification for a higher price becomes a reality, the world will be a “strange one” and “we’ll be lucky not to be bossed around by our automaton friends.”This “rather horrific” outlook is less likely than a crash, Grantham adds .”G

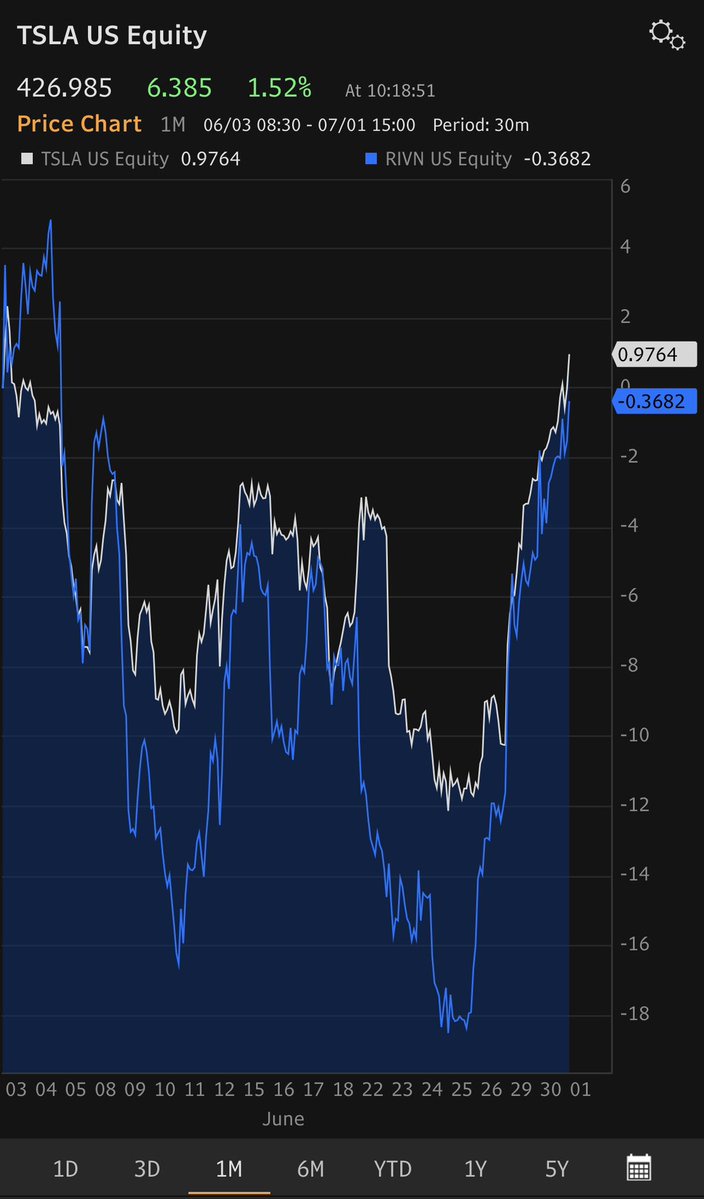

U.S. stocks rose pre-market Monday (SPX +0.4%, NDX +1.0%) as tech stocks rebounded ahead of this week’s Samsung and SK Hynix 2Q earnings, which will test the continuing viability of the AI trade. $Tesla(TSLA.US) recovered +1.3% pre-mkt after falling -7.5% Thursday and crushing Q2 deliveries (480K vs 406K est) amid surging 2Q gas prices as a result of the Iran conflict. Brent crude fell 1% to $71/bbl as Hormuz flows recovered. S&P 2026 EPS estimates have risen to $342 (+23% YoY), implying a 21.9x P/E and a 4.6% earnings yield, in line with 10-year treasury yields. I remain cautious on TSLA given likely commoditization of unsupervised autonomy in the coming year and a stretched valuation relative to forward earnings growth (6x PEG).

G

The avg price of a gallon of gas has risen from $2.98/gallon before the U.S.-Iran war to $3.86/gallon over the July 4th weekend after peaking at $4.56/gallon in June. The rise in gas prices is likely what caused the surge in 2Q EV deliveries YoY ( $Tesla(TSLA.US) +25%, $Rivian Automotive(RIVN.US) +14%, $Lucid(LCID.US) +20%) rather than recent advances in FSD/autonomy, which are still virtually unknown by most potential EV customers.

OPEC+ has a preliminary agreement for another modest oil quota increase in August, raising the prospect of more supply eventually hitting the market again if a US-Iran peace pact can stick. If ratified at a video conference on Sunday, seven major nations led by Saudi Arabia and Russia will add 188,000 barrels a day to their output target. The tiny on-paper hikes are starting to add up: it will mean they’ve added 940,000 barrels a day to quotas, equivalent to almost 1% of global demand, since the war began.Oil futures have tumbled 43% from their war-time peak of $118/barrel at the end of April to $72 a barrel today, with many forecasters predicting the re-emergence of a global glut. OPEC and its partners could soon face a choice between restraining output or fighting over market share via a potential price war. I expect $Tesla(TSLA.US) stock to rebound this week as the sell-side climbs over one another to increase 2Q and FY’26 earnings ests, which could boost TSLA price targets. That said, at a 2026 P/E of 200x+ vs +35% long-term (2027-2032) EPS growth, which equates to a 6x PEG vs 2x for $NVIDIA(NVDA.US), $Alphabet - C(GOOG.US), $Meta Platforms(META.US), $Broadcom(AVGO.US), etc., I continue to see $Tesla(TSLA.US) as fully-priced.G

+1

+1

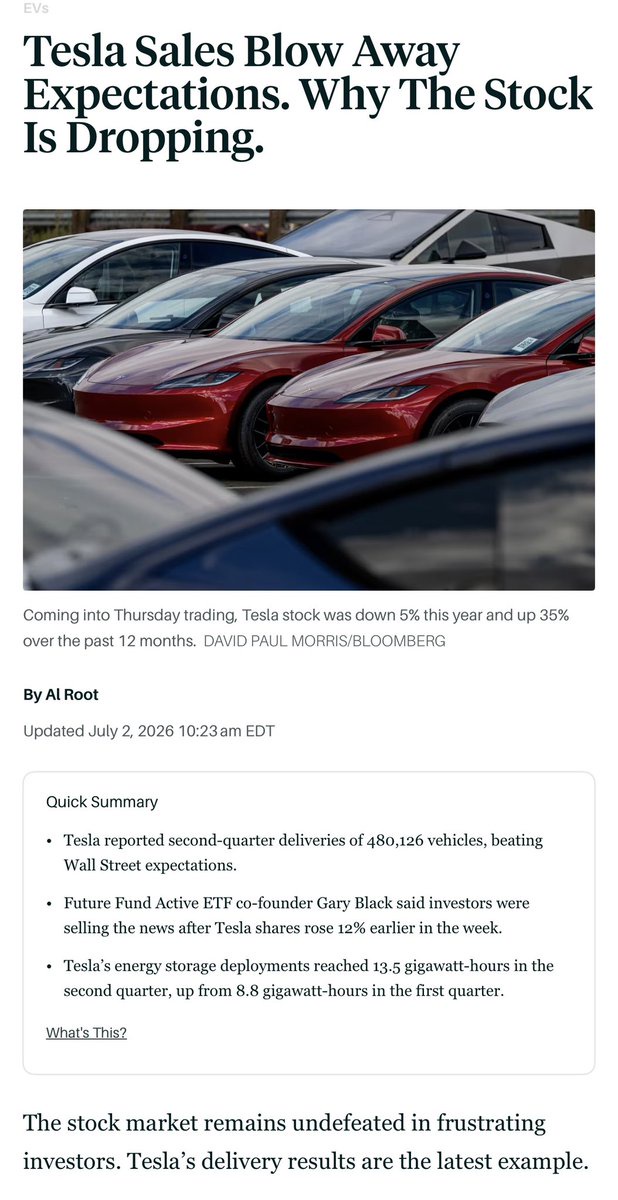

$Tesla(TSLA.US) (-7% today) blew away 2Q delivery ests. But investors anticipated the beat.

+1G

$Tesla(TSLA.US) (+0.7% pre-mkt) delivered 480K vehicles in 2Q, +25% YoY and far exceeding WS estimates of 406K. Excluding Models S and Y, which are being discontinued, TSLA 2Q delivs were 467K, and still +24% YoY. Days of inventory outstanding dropped from 29 DSO in 1Q to 17 DSO in 2Q.

G

U.S. stocks retreated pre-mkt (SPX -0.2%, NDX -0.8%) ahead of the June jobs report (+115K exp), with tech shares falling for a second day and South Korean chipmakers Samsung and SK Hynix plunging 9% and 13% respectively on oversupply concerns. Brent crude fell to $70.84/bbl amid high Strait of Hormuz flows, as Trump noted progress in U.S.-Iran negotiations. S&P 500 2026 EPS estimates have risen +23% YoY to $342 (2026 P/E 21.9x, 4.6% earnings yield vs 4.5% 10-year TYs) on AI and energy gains. TSLA 2Q deliveries are expected to beat consensus today (my est 420K vs WS est 406K) although my longer-term caution persists due to declining 2027-2030 earnings estimates, rising autonomous competition, and an extended valuation.

G

$Meta Platforms(META.US) +10% on a report from Bloomberg outlining plans to launch a cloud-infrastructure business to sell excess AI compute capacity.

The new business would increase competition between Meta and other technology conglomerates that have been spending big on AI development, including Amazon Web Services, Microsoft Azure and Google Cloud. Meta, like many of its competitors, is spending more and more on AI development. In its 1Q earnings report in April, Meta increased its projected 2026 capital spending to a range of $125B to $145B, up $10 billion. It cited "expectations for higher component pricing" and "additional data center costs."One potential plan includes selling access to various AI models that are hosted on Meta’s existing AI infrastructure, an approach similar to AWS’s Bedrock offering, the people said. Meta would run the data centers and chips that power the models, including its own Muse Spark models, and charge developers to access them. META is also considering selling access to “raw” computing capacity, akin to other so-called neocloud businesses like CoreWeave Inc. Development of these new business lines is part of Meta Compute, an internal initiative to build and manage the company’s AI infrastructure efforts. Meta has made developing AI “superintelligence” a top priority, and has committed hundreds of billions of dollars to data centers and other AI infrastructure. That investment has left investors anxious about Meta’s plans to earn a return on that spending, which includes major computing deals with CoreWeave, Google and Oracle Corp., among others. A cloud business offers one way to return some of that investment. AWS, Azure and Google Cloud have spent decades building platforms that rent access to computing power, storage and software over the internet — businesses that now command tens of billions of dollars per quarter in revenue.

G

$Tesla(TSLA.US) and $Rivian Automotive(RIVN.US) both rising into 2Q delivs tomorrow, throwing cold water on the idea that TSLA’s rise has to do with sudden excitement about FSD or AI. With 72% of TSLA profits and 100% of RIVN profits driven by sales of EVs, the likely delivs surprises tomorrow fueled by surging oil prices over the past quarter is clearly the reason for renewed optimism in both EV makers.

2Q Delivs Est: TSLA 406K, RIVN 10.6K

G

U.S. stocks were poised to open July cautiously (SPX -0.3%, NDX -0.6%) as investors await Fed Chair Kevin Warsh’s comments today at the ECB forum in Portugal for rate path clues amid rising price pressures and a strengthening economy. Brent crude -1%, 10yr yields -0.6bp to 4.46%, gold/silver were lower. S&P 2026 EPS estimates have risen to $342 (+23% YoY), implying a 21.8x P/E. $Tesla(TSLA.US) likely to beat WS 2Q delivery estimates tomorrow. We remain cautious on TSLA long-term due to declining earnings estimates, increased competition in unsupervised autonomy, and an extended valuation. $Nike(NKE.US) fell 3.4% pre-mkt after management again reduced 2027 rev guidance. The June U.S. employment report will be posted tomorrow before the market opens (+120K exp).

G

$Nike(NKE.US) -3.0% AH to $39.80 after posting 4Q revs and earnings that modestly beat WS consensus, excluding one time items. 2027 1Q rev and gross margin guidance will be announced on the earnings call which begins at 5pm ET.

4Q results:- EPS of $0.20 (excluding $.52 of one time tariff recovery) which beat analyst estimates of $.13.- Revs of $10.972B (-1.1% YoY) vs analyst consensus of $10.863B (-2% YoY). - At constant currency (CC), Nike revs -4.0% vs -3.9% exp- Gross margin 40.2% (excl 900bp of tariff recovery) vs 39.9% expected- Wholesale revs of $6.6B vs $6.5B est- Direct revs of $4.1B vs $4.1B est- North America in constant currency (CC) revs +3.0% YoY vs +3.1% exp- China revs -17.0% CC YoY vs -21.7% exp - Europe revs -6.0% CC YoY vs -5.0% expG

I expect $Tesla(TSLA.US) 2Q deliveries on Thursday morning to be ~410,000 (+7% YoY) and ahead of WS consensus of 406K after gas prices surged during the quarter. This could be TSLA’s 2nd consecutive YoY deliveries advance of >+5% after declining -9% in 2025 and -1% in 2024. We remain cautious on TSLA longer term as 2026-30 earnings ests continue to decline and as other manufacturers roll out unsupervised autonomy over the next 12 months. $Alphabet - C(GOOG.US) $Baidu(BIDU.US) $WeRide(WRD.US) $Pony AI(PONY.US) and $Amazon(AMZN.US) are now completing 1.0M paid unsupervised autonomous rides per week without safety monitors. We have no position in TSLA due to its extended valuation (2026 P/E 200x vs +35% long-term EPS growth, 6.0x PEG).

G

U.S. stocks were mixed pre-mkt, with the S&P 500 on track for its best quarter in six years amid a pending U.S.-Iran peace deal and AI momentum. Oil fell to $72.58/bbl, 10yr treasury yields dipped to 4.36%, while gold and silver rose. $NVIDIA(NVDA.US) inched higher and $Tesla(TSLA.US) retreated after yesterday’s +8% gain; $Aerovironment(AVAV.US) surged +20% on strong earnings. Traders have rotated back into long-duration AI/tech and recovering consumer names as inflation eases. S&P 2026 EPS estimates rose to $342 (+23% YoY), implying a 21.8x P/E. $Tesla(TSLA.US) Q2 deliveries are likely to beat on Thursday following the surge in gas prices during the quarter, though I remain cautious long-term due to declining 2027-2030 earnings estimates, intense autonomous competition, and a seemingly stretched valuation. $Nike(NKE.US) reports after the close today, and the June U.S. employment report comes out Friday.

G

$Aerovironment(AVAV.US) +15% after hours after beating 4Q ests and guiding to higher than consensus FY’27 revs. FY’27 guidance for Adj EBITDA and Adj EPS were below expectations although the company has a history of guiding conservatively at the beginning of the fiscal year. AVAV had declined -42% YTD after missing 3Q revs and cutting full-year 2026 rev and EBITDA guidance.

AVAV designs and produces drones, tracking antenna, sensors, and missiles for government agencies and businesses that sell to the U.S. Department of Defense. Short interest is 12.6% of float.4Q results:- Revs $641.6M vs $558.8M est- Adj EBITDA $140.1M vs $126.1M est- Adj EPS $1.84 vs $1.41 est- Backlog $1.2B vs $1.077B estFY’27 Guidance:- Revs $2.13B - $2.23B vs $2.16B est- Adj EBITDA $305M-325M vs $346M est- Adj EPS $3.02-$3.39 vs $3.79 estConf call at 430pm ETG

+1

+1

$Tesla(TSLA.US) -15% year-to-date (vs NDX +16%) as TSLA’s rollout of unsupervised autonomous driving continues to sputter. TSLA bull Dan Ives continues to predict that TSLA is on its way to $600 with numerous catalysts. We remain skeptical with TSLA’s unsupervised autonomy fleet (no safety monitors) seemingly stalled at around 40 vehicles until efficacy improves. Many TSLA bulls erroneously count supervised autonomous vehicles (which employ safety monitors in the front seat) in their TSLA fleet numbers which is misleading.

Earlier this month, the tragic accident outside Houston where a driver who said FSD was engaged plowed into a house killing the owner inside, combined with the absence of TSLA PR unleased a torrid of negative media headlines. We continue to battle with TSLA bulls on the shortsightedness of not investing in PR even as TSLA management accused the media of lying. This is akin to a dad blaming the school if his son didn’t make the football team even though his kid didn’t bother to try out. We expect TSLA to continue to underperform (1yr TSLA +19% vs NDX +28%, 3yr TSLA +48% vs NDX +95%, 5yr TSLA +67% vs NDX +99%) until TSLA can scale up its unsupervised autonomous fleet (no safety monitors) from the current 40 vehicles to areas representing 50% of the U.S. population as targeted by Elon Musk on July 23 2025 during Tesla’s Q2 2025 earnings call: (“I think we’ll probably have autonomous rides -hailing in probably half the population of the U.S. by the end of the year [2025]).” I expect TSLA to continue to underperform NDX until unsupervised autonomy scales. I don’t see that happening until FSD efficacy reaches 99.99% (1 intervention every 10,000 drives). Today TSLA FSD efficacy is probably 99% (1 intervention every 100 drives). TSLA bulls also seem to be latching onto the silly idea that $SpaceX(SPCX.US) with a market cap of $2 trillion will somehow use its expensive stock to buy TSLA with its $1.4 trillion market cap, despite potential massive dilution (we est ~25% dilution at existing market caps and multiples) and obvious governance questions.In 2Q we expect TSLA and other EV makers to benefit from stubbornly high gas prices which should boost EV deliveries. On Friday, TSLA IR posted its 2Q consensus delivery estimates which show a 2Q delivery gain of +6% YoY and FY 26 delivery gain of +1% YoY, which suggests TSLA deliveries could avoid a third consecutive year of decline. While bulls argue that TSLA is not just a car company, EVs still make up 72% of TSLA gross profits and it’s difficult to expect investors to accord a 200x P/E to a stock with earnings that are shrinking and its unsupervised autonomy rollout stalled.+1