BIDU: Little Else to Lean On — All in on Kunlun chips

$Baidu(BIDU.US) Q1 was a mixed bag, reflecting a sharp strategic pivot and business transition. Investors now care less about the long-troubled ads business and more about whether the AI Cloud, Kunlun Chip and buybacks can execute smoothly.

Last quarter the company switched to a new disclosure framework, splitting into 'AI biz.' and 'Legacy biz.'. AI includes AI Infra, AI Application and AI-native Marketing Services. Since most Street models still follow the old framework, Dolphin Research maps the two to show both the expectation gap and growth across BIDU's new AI lines.

Specifically (Baidu Core only, ex-iQIYI): The focus below is on Baidu Core and excludes iQIYI. We highlight the key moving parts for revenue and profit.

1) AI now accounts for over half of revenue: AI-related revenue reached RMB 13.6bn in Q1, or 52% of total, up from 43% in Q4. The mix shift toward AI continued to accelerate.

(1) AI Infra (cloud, LLM API, compute leasing) is the real backbone: Revenue came in at RMB 8.8bn, roughly two-thirds of AI revenue, up 79% YoY and ahead of consensus. GPU cloud rose 183% and was the core growth engine.

(2) AI applications (Baidu Wenku, Netdisk and digital employees) weakened further QoQ. Stripping out drag from Netdisk, pure AI apps like digital employees also slowed, which looks out of sync with sector sentiment and likely reflects intensifying competition.

(3) AI-native marketing (agents and digital humans) also softened QoQ. This likely faces the same competitive pressure as the digital employee product line.

2) Legacy ads remain on the floor, as expected: Traditional ads (search, feed ads, etc.) fell 28% YoY, worsening from -26% in Q4. Holiday timing played a role, but sector weakness and BIDU's eroding competitiveness also hurt, with Mobile Baidu MAU down another 22mn QoQ in Q1, making a near-term inflection hard to envision.

3) Autonomous driving, smart devices and others: This bucket delivered RMB 2.1bn in Q1, down QoQ. Robotaxi completed 3.2mn orders in Q1, up 120% YoY.

Due to Mainland regulatory constraints, Apollo has focused on overseas markets since H2 last year. After tests in the Middle East, the U.K. and Korea, highway testing is now progressing in Switzerland, with Dubai the fastest where operations have started and the Robobus app launched locally in Mar.

Apollo now covers 27 cities globally. This asset could also be carved out and capitalized in the future.

4) Costs down on restructuring: Last quarter already showed sizable workforce optimization (c.RMB 700mn in severance). In Q1, opex fell 10%, taking opex/revenue down to 31% from 45% in Q4.

SBC also fell 24% YoY in Q1. With the market cap higher vs. last year, this implies a sharp reduction in total award recipients.

Despite a sharp decline in high-margin ads, OP improved QoQ but still fell YoY. Relative to expectations, the scale of cost tightening surprised to the upside.

5) Higher investment, buyback on plan: Capex nearly doubled YoY to RMB 5.8bn in Q1. Even so, it remains low vs. other LLM/cloud leaders, and AI Infra revenue of RMB 8.8bn fully covers capex.

Under the 2-yr $5bn buyback announced in Feb, BIDU repurchased $172mn in Q1 (roughly one month), a pace that looks a bit light. We will watch management's plans for the rest of the year on the call.

Management appears more focused on shareholder returns than before, and BIDU holds nearly RMB 100bn of net cash (ex short-term borrowings). Cash flow is ample to fund buybacks and capex over the next two years.

The implied shareholder yield is still around 5–6% before dividends. If the buyback runs at the cap, $2.5bn per year compares with a ~$46bn market cap.

6) Kunlun Chip IPO approaching: Kunlun filed for IPO guidance in early May. Based on typical HK procedures, an early listing window could be Jul–Aug, and as domestic compute is a hot theme this year, Kunlun's IPO should offer a near-term catalyst for BIDU's valuation.

7) Detailed financials at a glance

Dolphin Research View

AI Cloud is what can carry BIDU near term, including LLM API, compute leasing and the Kunlun chip stack. The sector backdrop remains strong, lifting most vendors regardless of product gaps.Among these, Kunlun looks the most competitive and offers the most upside optionality.

What could Kunlun be worth? Dolphin Research ran the math in the early-year note 'Kunlun IPO Accelerates: BIDU’s Google Moment?'. The framework remains broadly valid.

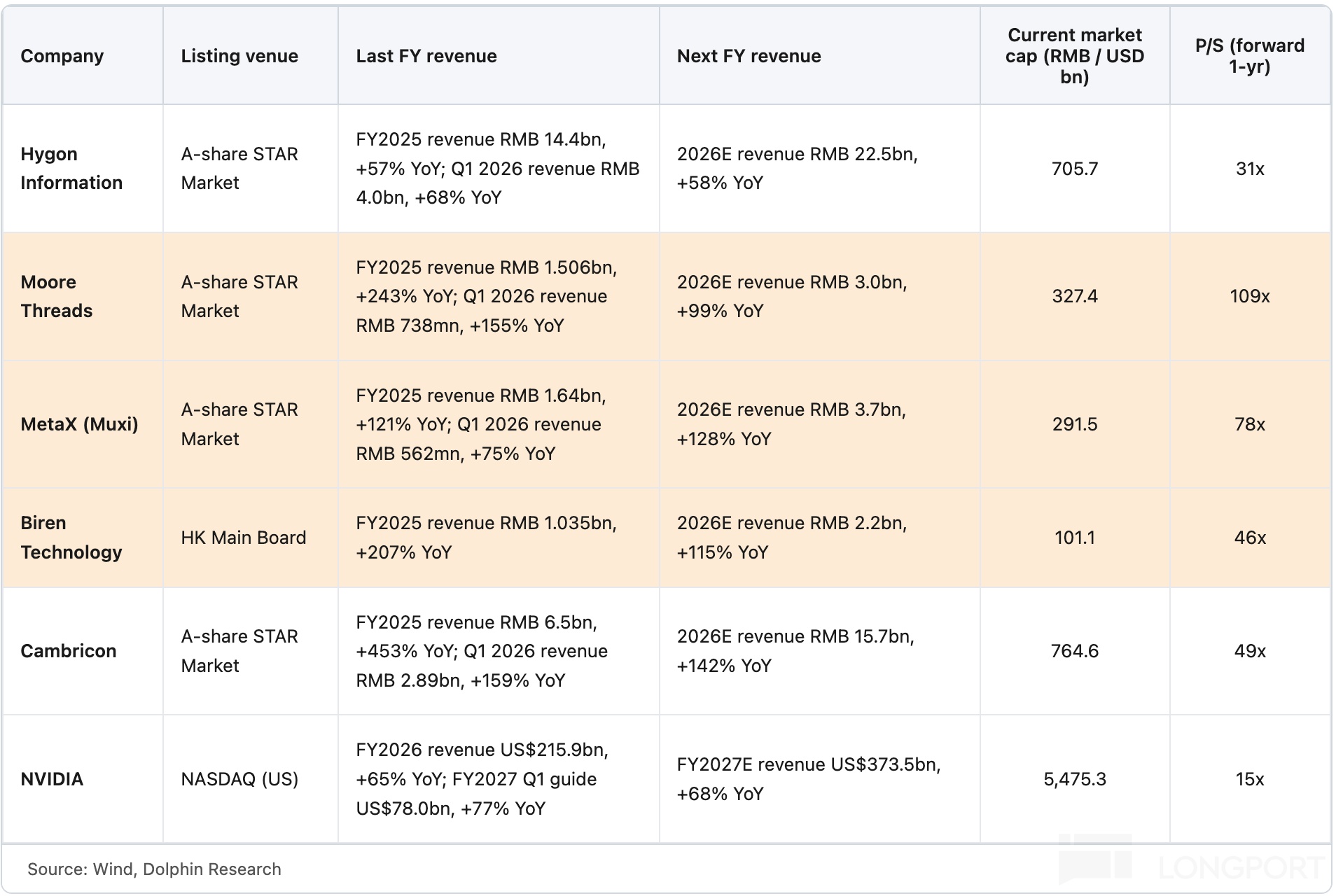

(1) There is not much change in the operating outlook so far, though Street revenue expectations are ~RMB 6–7bn, making our prior RMB 8.4bn look optimistic. Upside risks include Samsung capacity constraints and potential pricing pressure in H2 as rival shipments bunch up amid performance gaps.

(2) Versus listed domestic GPU peers, a 15x P/S looks conservative. Kunlun is ASIC while the 'Big Four' use GPGPU architectures, yet the end goal for customers is similar.Clients ultimately benchmark chips on performance, stability and price.

Kunlun's R&D and supply-chain execution are not behind peers, and it has ample HBM reserved to support shipments. Current orders are mainly from internal use at BIDU, plus Tencent, China Mobile, Geely, China Southern Power Grid and China Merchants Bank. With BIDU pivoting harder to AI Cloud this year, Kunlun is well placed to capture the current upcycle.

The more the BIDU story leans on Kunlun, the more the valuation needs Kunlun's catalysts. Without progress and fresh positive news, the stock will likely drift with the market and get pulled back by legacy-biz logic.

Opportunity still clusters around the Kunlun IPO window, i.e., Q3. On valuation, the current ~$46bn market cap implies ~21x 2026E P/E, which screens rich vs. China ADR peers, but as the IPO nears, SOTP becomes more appropriate.

(1) Ads (incl. AI-native marketing): assign 4x P/E on RMB 56.5bn revenue (-10%), 30% OPM and 15% effective tax to get ~$8.3bn. This embeds further weakness and execution risk in the legacy engine.

(2) Kunlun: on RMB 7.5bn revenue, 40x P/S, 59% ownership and a 30% holdco discount, we get ~$13bn. This reflects scarcity and the near-term listing catalyst.

(3) Cloud ex-Kunlun: assume +20% to RMB 43.6bn revenue. At 4x P/S, that suggests ~$25.5bn.

<1–3> sum to ~$46.6bn, essentially in line with the current ~$46bn. Some institutions also value Robotaxi separately and add net cash and the iQIYI stake.

Dolphin Research thinks that approach embeds peer-premium risk: add Robotaxi only when there is a concrete spin move. The iQIYI stake is volatile on weakened fundamentals and fits only in a bullish case.Adding all net cash is also not reasonable; at most add the $5bn buyback plan, implying a 5–6% shareholder yield.

In early trading after Kunlun's listing, if macro sentiment holds and BIDU advances a dual-primary listing, a short-term spike is possible. That will be more about trading timing.

Deep Dive

I. Biz. structure

BIDU is unusual among internet names in giving highly granular splits: 1) Baidu Core covers legacy ads (search/feed) and new initiatives (Intelligent Cloud/DuerOS smart speakers/Apollo), plus AI revenue across AI Infra (cloud, LLM API, compute leasing), AI Application (Baidu Wenku, Netdisk, digital employees) and AI-native marketing (agents and digital humans). The framework clarifies growth and profitability drivers.

2) iQIYI: membership, ads and content sublicensing. Disclosures are detailed as it is separately listed.

The two are cleanly separated, and iQIYI has standalone data for triangulation. There is ~1% (RMB 200–400mn) intercompany offset between the two, so our Baidu Core rebuild may differ slightly from reported figures, but the trends are unaffected.

II. AI contribution rose to 52%

Baidu Core revenue was RMB 26.0bn (+2% YoY). AI growth essentially offset declines in legacy businesses.

(1) AI biz. After a year of ramp, AI Infra is the true pillar, with GPU cloud as the engine. The real demand is for compute, and BIDU's full-stack AI with integrated soft/hard capabilities remains relatively scarce.

AI apps derived from LLMs appear to have hit a near-term ceiling, with both AI applications (Wenku, Netdisk, digital employees) and AI-native ads (agents, digital humans) flat to weakening QoQ. Momentum has clearly cooled.

(2) Legacy biz. There is little to add here, as the market does not expect a near-term turn. In Q1, Mobile Baidu lost the AI-portal traffic battle and kept shedding MAUs, with even seasonal strength failing to help.

Recasting into the old framework for comparison: (1) Ads fell 21.5% YoY, with traditional ads down 28%. Holiday timing played a part, but underlying pressure remains.

(2) Cloud and other revenue rose 42% YoY off a high base, beating expectations. AI-driven demand underpinned the strength.

III. Higher capex, leaner headcount

BIDU made sizeable org changes late last year to integrate legacy ops, drive efficiency, and dedicate owners for each AI sub-line. Last quarter was a transition; this quarter already shows tangible effects.

(1) Core GPM fell to 44% as ads weakened and AI cloud mix rose. The mix shift weighed on margins.

(2) Core OP was RMB 3.4bn with a 13% OPM, reflecting the early impact of layoffs. S&M and R&D fell 17% and 4%, respectively.

IV. Capex expanding, more room to go

Q1 FCF turned negative as capex nearly doubled YoY to RMB 5.8bn. That is still modest vs. other LLM/cloud leaders, and AI Infra revenue of RMB 8.8bn fully covers capex.

Part of this reflects cost advantages from BIDU's full-stack AI and in-house chips. Given the cash buffer and sector heat, BIDU has room to lean in more aggressively.

<End here>

Dolphin Research on 'Baidu' – Past Notes:

Recent earnings season

Feb 26, 2026 Trans 'Baidu (Trans): Sharper Focus on Shareholder Returns and Execution'

Feb 26, 2026 Results Review 'Baidu: Ad Moat Eroded, Is Kunlun the Lifeline?'

Nov 18, 2025 Trans 'Baidu (Trans): AI-Native Marketing as the Second Growth Curve'

Nov 18, 2025 Results Review 'Talking Up AI Hard — Can Baidu Be Saved?'

Risk Disclosure & Statement: Dolphin Research Disclaimer and General Disclosure

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.