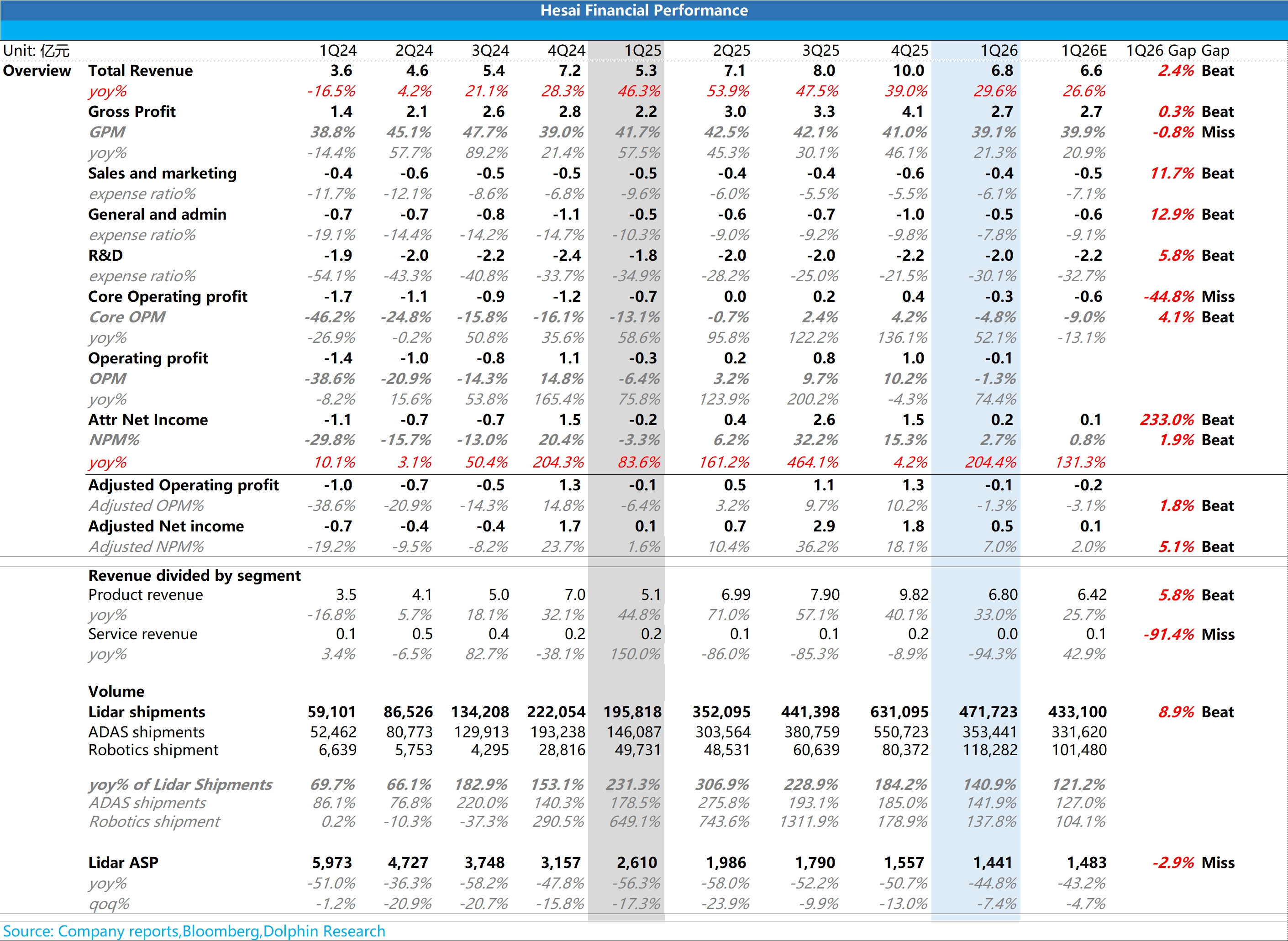

HSAI 1Q26 First Take: Slight beat overall, with revenue above the midpoint of guidance, but core OP remained in the red as ASP deflation weighed on margins.

1) Revenue: higher volume, lower price, slight beat

Revenue was RMB 684 mn (+28.7% YoY), landing toward the upper end of the RMB 650–700 mn guide. Growth was fully driven by shipments beating plan.

Shipments beat: seasonally soft quarter proved resilient, with ADAS and robotics as dual drivers.

Q1 is typically off-season, compounded by the phase-down of domestic NEV purchase tax incentives (domestic NEV sales -4% YoY), yet total shipments reached 477k units vs. 400–450k guided. This again underscores accelerating LiDAR penetration into mid- to lower-end models.

ADAS shipments were 353k units (+142% YoY), led by the thousand-yuan ATX ramping in RMB 100k–200k models at BYD and Geely. The lower-priced blind-spot filler FTX also started to scale.

Robotics shipments were 124k units (+138% YoY), exceeding the 100k guide. Growth was driven by the JT series for lawn mowers and related use cases.

② ASP still deflating: intensified competition as the main driver

Blended ASP was about RMB 1,441, down 45% YoY and a further 7% QoQ vs. 4Q25. Despite a higher mix of higher-priced robotics LiDARs (up 13ppt QoQ to 25%), overall ASP was dragged down, reflecting both mix and price-for-volume competition.

a. Mix shifted toward lower-priced ATX (e.g., custom versions supplied to BYD and Geely) with unit price around RMB 800. This is well below the 2026 overall ATX Avg. of about USD 150.

b. The lower-priced FTX blind-spot filler (about USD 100) began to ship. This further pushed down blended ASP.

2) Gross margin: notably pressured, GPM fell below the key 40% threshold for the first time

GPM was 39.1%, down 260bps YoY, below the market’s 39.9% expectation and the company’s usual 40%+ level. This marks a break below a psychologically important line.

The decline was mainly because ASP deflation (-45% YoY) outpaced cost reductions from in-house chips, with scale benefits not yet realized. As a result, per-unit GP was under pressure.

3) Opex and profit: disciplined spend, but core OP still loss-making

Q1 opex totaled RMB 300 mn; against ~30% revenue growth, opex rose ~40% YoY, reflecting tighter internal management and a more refined operating approach. Cost control remained a focus despite growth investments.

Core OP came in at -RMB 30 mn, a small loss as ASP deflation compressed GP and seasonality limited scale leverage. Still, it was slightly better than the market expected. $Hesai(HSAI.US) $Hesai(HSAI.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.